Sustainability Concept in Decision-Making: Carbon Tax Consideration for Joint Product Mix Decision

Abstract

:1. Introduction

2. Literature Review

2.1. Carbon Tax

2.2. Concepts of ABC and TDABC

2.3. Applying TOC and ABC to Product Mix Decision-Making

2.4. The Pharmaceutical Industry Joint Product Mix Decision-Making

3. Models for Joint Product Mix

3.1. Notations

3.1.1. Decision Variables

- is the company’s profit;

- is the quantity of material APIs for the production of the joint product;

- is the production quantity of joint product at the split-off point;

- is the quantity of joint product processed further in a separate process after the split-off point;

- is the units of product for each unit of joint production (coefficient of the joint production);

- is the units of products produced by processing each unit of products after the split-off point (coefficient of processing production after the split-off point);

- is the batches of joint products;

- is the batches of products processed after the split-off point;

- is the quantity of a shipment of joint product ;

- is the quantity of a shipment of product processed further in a separate process after the split-off point;

- is the demand for joint product ;

- is the demand of product after the split-off point;

- is the tableting department labor/hour production capacity;

- is the production capacity of tableting machine operating hours;

- is the order processing and tableting control department production capacity;

- is the shipping department production capacity;

- is the pharmaceutical inspection capacity;

- is the VOCs’ disposal capacity;

- is a zero, one variable; if joint product is not produced, it is zero; otherwise, it is one;

- is a zero, one variable; if product is processed further in a separate process, but is not produced after the split-off point, it is zero; otherwise, it is one.

3.1.2. Parameters

- is the unit price of joint product at the split-off point;

- is the unit price of joint product processed further in a separate process after the split-off point;

- MA0 is the unit price of material APIs for the production of the joint product;

- MAi1 is the unit price of material APIs for the further processing of the joint products;

- is the marketing, plant guard and management costs;

- is the direct labor hours demanded for the production of joint product ;

- is the direct labor hours demanded for the production of product processed further in a separate process after the split-off point;

- is the hours for the operation of the tableting machine for the production of joint product ;

- is the hours required for the processing and production of product after the split-off point;

- is the time to initiate the tableting machine for joint product ;

- is the time to initiate the tableting machine for joint product processed further in a separate process after the split-off point;

- is the time of order processing of joint product ;

- is the time of order processing of joint product processed further in a separate process after the split-off point;

- is the time to shift each batch of APIs for joint product to the tableting department;

- is the time to shift each batch of APIs for joint product processed further in a separate process after the split-off point to the tableting department;

- is the time to ship joint product ;

- is the time to ship product processed further in a separate process after the split-off point;

- is the time to package each unit of joint product ;

- is the time to package each unit of joint product processed further in a separate process after the split-off point;

- is the time for inspection of joint product ;

- is the time for inspection of product processed further in a separate process after the split-off point;

- is the time for the disposal of each batch of volatile organic compounds (VOCs) produced in the production of joint product ;

- is the time to for the disposal of each batch of volatile organic compounds (VOCs) produced in the production of product processed further in a separate process after the split-off point;

- is the quantity of joint product of each batch;

- is the quantity of joint product of each batch;

- is the quantity of each shipment of joint product ;

- is the quantity of each shipment of product ;

- is the unit labor hourly costs of the tableting department;

- is the unit tableting machine’s operating cost per hour;

- is the unit labor/hour costs of the order processing department;

- is the unit labor/hour costs of the shipping department;

- is the unit pharmaceutical inspection hourly cost.

3.2. The TDABC Model

3.3. TOC Model

3.4. ABC Model

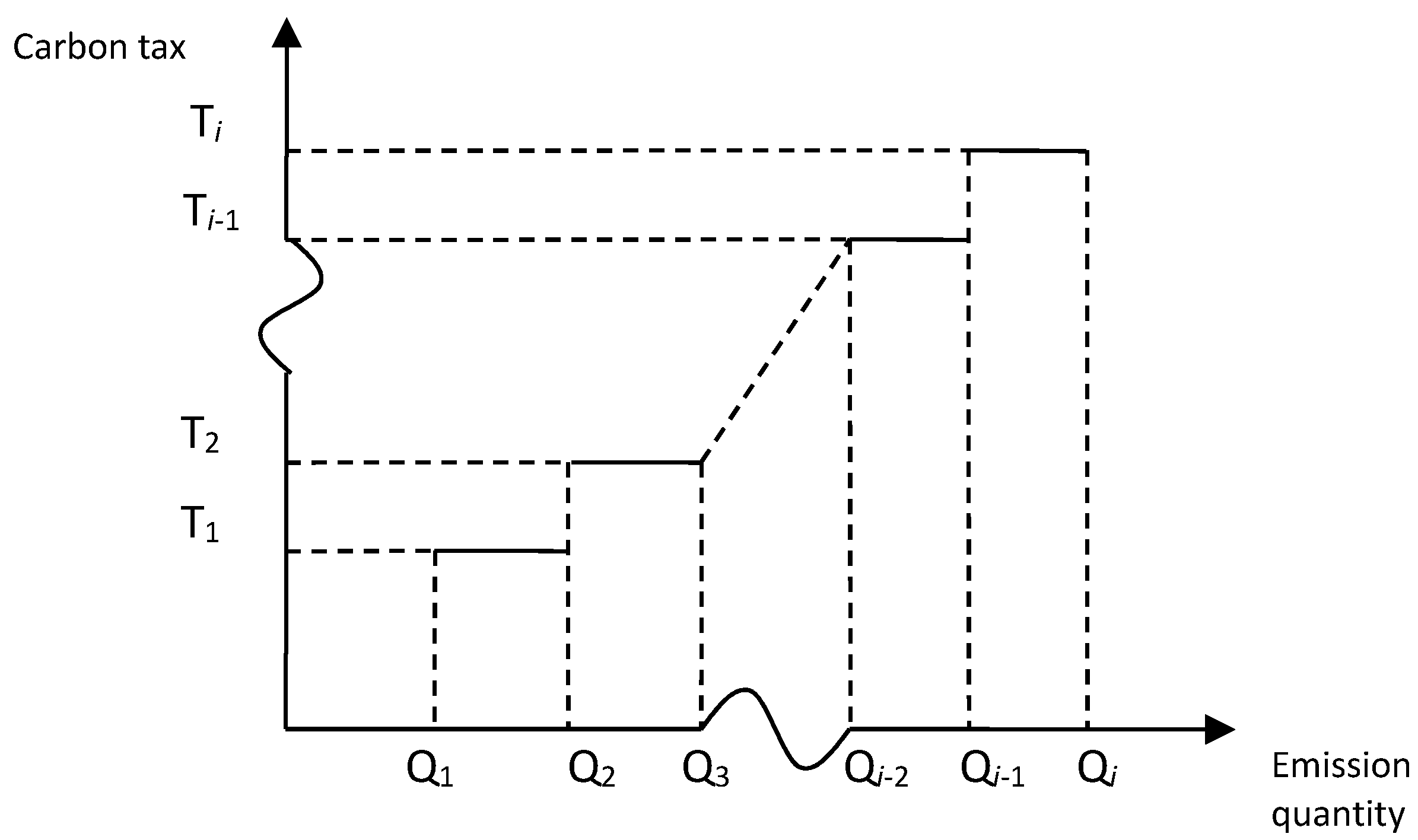

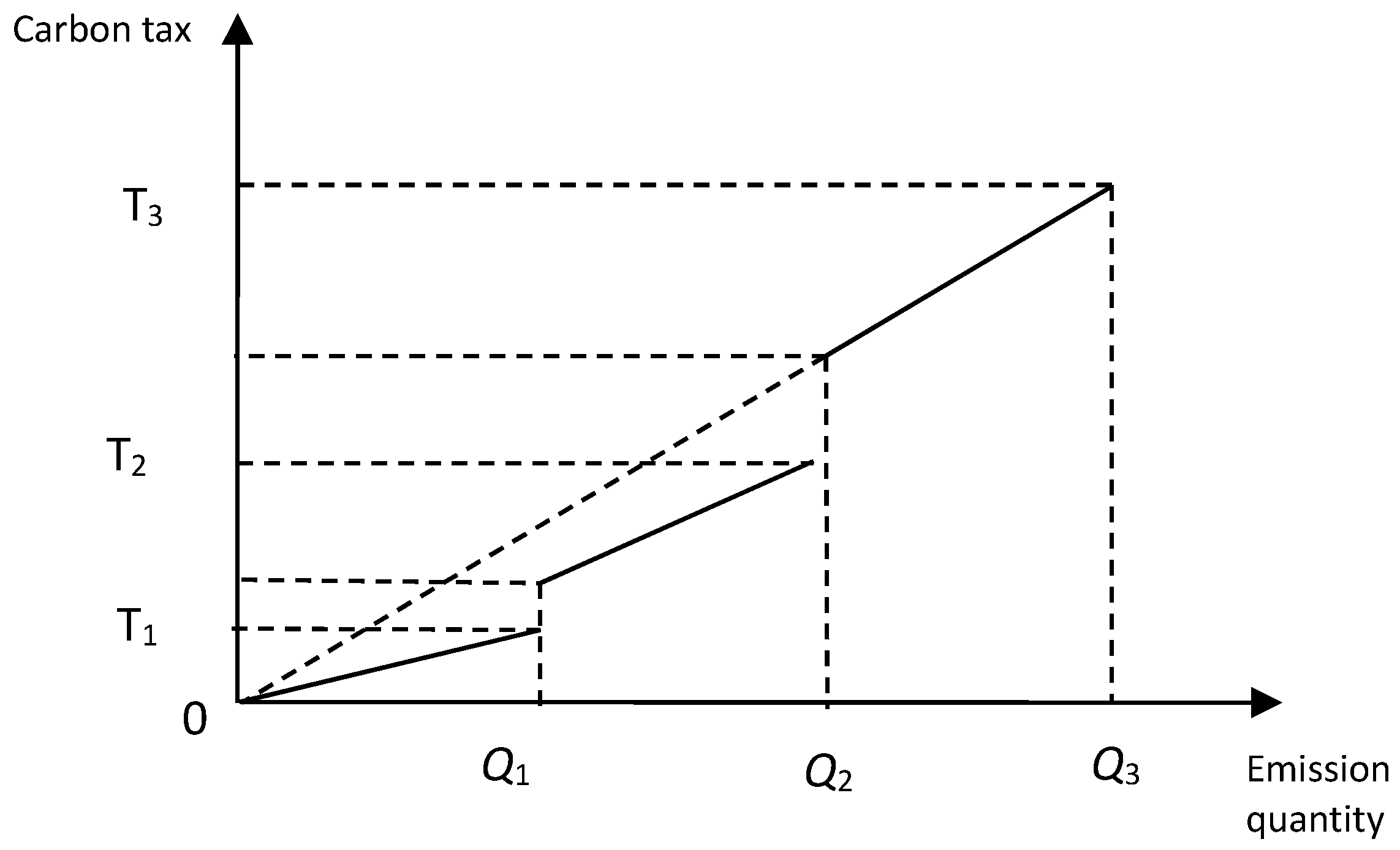

3.5. Sensitivity Test with Carbon Tax

- is the carbon tax rate of the r-th carbon emission charge level;

- is the upper limit of the r-th carbon emission charge level;

- is a zero/one variable; means that the carbon emission quantity is within the r-th carbon emission charge level;

- are the variable for the carbon emission quantity within the first, second and third carbon emission charge levels, respectively.

4. An Illustrative Case

4.1. TDABC

4.2. TOC

4.3. ABC

4.4. Analysis

4.5. Sensitivity Test with Carbon Tax

5. Discussion

6. Conclusions

Acknowledgments

Author Contributions

Appendix A

{kind=link}

{kind=link}

{kind=link}

| Subject to Direct Material | Subject to Tableting Labor Subject to Tableting Machinery |

| Subject to Inspection Subject to VOCs Disposal | Subject to Ordering Subject to Shipping |

| Optimal Joint Product Mix Solution for the TDABC Model | |

| Subject to Direct Material | Subject to Tableting Labor Subject to Tableting Machinery |

| Subject to Inspection Subject to VOCs Disposal | Subject to Ordering Subject to Shipping |

| Optimal Joint Product Mix Solution for the TDABC Model | |

| Subject to Direct Material Subject to Ordering | Subject to Tableting Labor Subject to Tableting Machinery |

| Subject to Inspection Subject to VOCs Disposal | Subject to Shipping |

| Optimal Joint Product Mix Solution for the TDABC Model | |

| Subject to Direct Material | Subject to Tableting Labor Subject to Tableting Machinery |

| Subject to Inspection Subject to Carbon Tax | Subject to Ordering Subject to Shipping Subject to VOCs Disposal |

| Sensitivity Analysis of TDABC Model with the Carbon Tax | |

References

- Tsai, W.H.; Lai, C.W.; Tseng, L.J.; Chou, W.C. Embedding management discretionary power into an ABC model for joint product mix decisions. Int. J. Prod. Econom. 2008, 115, 210–220. [Google Scholar]

- Tsai, W.H. Activity-based costing model for joint products. Comput. Ind. Eng. 1996, 31, 725–729. [Google Scholar]

- Hartley, R.V. Decision making when joint products are involved. Account. Rev. 1971, 46, 746–755. [Google Scholar]

- Kee, R.; Schmidt, C. A comparative analysis of utilizing activity-based costing and the theory of 3 constraints for making product-mix decisions. Int. J. Prod. Econom. 2000, 63, 1–17. [Google Scholar] [CrossRef]

- Onwubolu, G.C.; Muting, M. Optimizing the multiple constrained resources product mix problem using genetic algorithms. Int. J. Prod. Res. 2001, 39, 1897–1910. [Google Scholar] [CrossRef]

- Tsai, W.-H.; Lee, K.-C.; Liu, J.-Y.; Lin, H.-L.; Chou, Y.-W.; Lin, S.-J. A mixed activity-based costing decision model for green airline fleet planning under the constraints of the European Union Emissions Trading Scheme. Energy 2012, 39, 218–226. [Google Scholar] [CrossRef]

- Kirche, E.; Srivastava, R. An ABC-based cost model with inventory and order level costs: A comparison with TOC. Int. J. Prod. Res. 2005, 43, 1685–1710. [Google Scholar] [CrossRef]

- Gong, Z.; Hu, S. An economic evaluation model of product mix flexibility. Omega 2008, 36, 852–864. [Google Scholar]

- Turney, P.B. Common Cents: The ABC Performance Breakthrough: How to Succeed with Activity-Based Costing; Cost Technology: Hillsboro, OR, USA, 1991. [Google Scholar]

- Plenert, G. Optimizing theory of constraints when multiple constrained resources exist. Eur. J. Oper. Res. 1993, 70, 126–133. [Google Scholar] [CrossRef]

- Souren, R.; Ahn, H.; Schmitz, C. Optimal product mix decisions based on the theory of constraints. Exposing rarely emphasized premises of throughput accounting. Int. J. Prod. Res. 2005, 43, 361–374. [Google Scholar] [CrossRef]

- Fredendall, L.D.; Lea, B.R. Improving the product mix heuristic in the theory of constraints. Int. J. Prod. Res. 1997, 35, 1535–1544. [Google Scholar] [CrossRef]

- Pernot, E.; Roodhooft, F.; Van den Abbeele, A. Time-driven activity-based costing for inter-library services: A case study in a university. J. Acad. Librariansh. 2007, 33, 551–560. [Google Scholar] [CrossRef]

- Szychta, A. Time-Driven Activity-Based Costing in Service Industries. Soc. Sci. 2010, 67, 49–60. [Google Scholar]

- Stouthuysen, K.; Swiggers, M.; Reheul, A.-M.; Roodhooft, F. Time-driven activity-based costing for a library acquisition process: A case study in a Belgian University. Lib. Collect. Acquis. Tech. Serv. 2010, 34, 83–91. [Google Scholar] [CrossRef]

- Öker, F.; Adigüzel, H. Time-driven activity-based costing: An implementation in a manufacturing company. J. Corp. Account. Financ. 2010, 22, 75–92. [Google Scholar] [CrossRef]

- Tsai, W.-H.; Shen, Y.-S.; Lee, P.-L.; Chen, H.-C.; Kuo, L.; Huang, C.-C. Integrating information about the cost of carbon through activity-based costing. J. Clean. Prod. 2012, 36, 102–111. [Google Scholar] [CrossRef]

- Friedman, M. The Social Responsibility of Business Is to Increase Its Profits. The New York Times Magazine, 13 September 1970. [Google Scholar]

- Carroll, A.B. The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Bus. Horiz. 1991, 34, 39–48. [Google Scholar] [CrossRef]

- Tsai, W.-H.; Chen, H.-C.; Leu, J.-D.; Chang, Y.-C.; Lin, T.W. A product-mix decision model using green manufacturing technologies under activity-based costing. J. Clean. Prod. 2013, 57, 178–187. [Google Scholar] [CrossRef]

- Demeere, N.; Stouthuysen, K.; Roodhooft, F. Time-driven activity-based costing in an outpatient clinic environment: Development, relevance, and managerial impact. Health Policy 2009, 92, 296–304. [Google Scholar] [CrossRef] [PubMed]

- Tsai, W.-H.; Yang, C.-H.; Chang, J.-C.; Lee, H.-L. An Activity-Based Costing Decision Model for Life Cycle Assessment in Green Building Projects. Eur. J. Oper. Res. 2014, 238, 607–619. [Google Scholar] [CrossRef]

- Cooper, R.; Kaplan, R.S. Measure costs right: Make the right decisions. Harv. Bus. Rev. 1988, 66, 96–103. [Google Scholar]

- Tsai, W.-H.; Hung, S.-J. A Fuzzy Goal Programming Approach for Green Supply Chain Optimisation under Activity-Based Costing and Performance Evaluation with a Value-chain Structure. Int. J. Prod. Res. 2009, 47, 4991–5017. [Google Scholar] [CrossRef]

- Tsai, W.-H.; Hsu, J.-L.; Chen, C.-H.; Chou, Y.-W.; Lin, S.-J.; Lin, W.-R. Application of ABC in hot spring country inn. Int. J. Manag. Enterp. Dev. 2010, 8, 152–174. [Google Scholar] [CrossRef]

- Kaplan, R.S.; Cooper, R. Cost & Effect: Using Integrated Cost Systems to Drive Profitability and Performance; Harvard Business School Press: Boston, MA, USA, 1998. [Google Scholar]

- Kaplan, R.S.; Anderson, S.R. Time-driven activity-based costing. Harv. Bus. Rev. 2004, 82, 131–140. [Google Scholar] [CrossRef] [PubMed]

- Kaplan, R.; Anderson, S.R. Time-Driven Activity-Based Costing: A Simpler and More Powerful Path to Higher Profits; Harvard Business School Press: Boston, MA, USA, 2013. [Google Scholar]

- Stouthuysen, K.; Schierhout, K.; Roodhooft, F.; Reusen, E. Time-driven activity-based costing for public services. Public Money Manag. 2014, 34, 289–296. [Google Scholar] [CrossRef]

- Öker, F.; Özyapici, H. A New Costing Model in Hospital Management: Time-Driven Activity-Based Costing System. Health Care Manag. 2013, 32, 23–36. [Google Scholar] [CrossRef] [PubMed]

- Varila, M.; Seppänen, M.; Suomala, P. Detailed cost modelling: A case study in warehouse logistics. Int. J. Phys. Distrib. Logist. Manag. 2007, 37, 184–200. [Google Scholar] [CrossRef]

- Kaplan, R.S.; Norton, D.P. Mastering the management system. Harv. Bus. Rev. 2008, 86, 62–77. [Google Scholar] [PubMed]

- Huang, S.-Y.; Chen, H.-J.; Chiu, A.-A.; Chen, C.-P. The application of the theory of constraints and activity-based costing to business excellence: The case of automotive electronics manufacture firms. Total Q. Manag. Bus. Excell. 2014, 25, 532–545. [Google Scholar] [CrossRef]

- Tsai, W.-H.; Chou, W.-C. Selecting Management Systems for Sustainable Development in SMEs: A Novel Hybrid Model Based on DEMATEL, ANP, and ZOGP. Expert Syst. Appl. 2009, 36, 1444–1458. [Google Scholar] [CrossRef]

- Goldratt, E.M.C.J. The Goal: A Process of Ongoing Improvement; Creda Press: Cape Town, South Africa, 1984. [Google Scholar]

- Aryanezhad, M.; Komijan, A. An improved algorithm for optimizing product mix under the theory of constraints. Int. J. Prod. Res. 2004, 42, 4221–4233. [Google Scholar] [CrossRef]

- Kee, R. The sufficiency of product and variable costs for production-related decisions when economies of scope are present. Int. J. Prod. Econom. 2008, 114, 682–696. [Google Scholar] [CrossRef]

- Tsai, W.-H.; Lai, C.-W.; Chang, J. An algorithm for optimizing joint products decisions, as based on the Theory of Constraints. Int. J. Prod. Res. 2007, 45, 3421–3437. [Google Scholar] [CrossRef]

- Tsai, W.-H.; Lai, C.-W. Outsourcing or capacity expansions: Application of activity-based costing model on joint products decisions. Comput. Oper. Res. 2007, 34, 3666–3681. [Google Scholar] [CrossRef]

- Tehrani Nejad Moghaddam, A.; Michelot, C. A contribution to the linear programming approach to joint cost allocation: Methodology and application. Eur. J. Oper. Res. 2009, 197, 999–1011. [Google Scholar] [CrossRef]

- Tsai, W.-H.; Lin, S.-J.; Liu, J.-Y.; Lin, W.-R.; Lee, K.-C. Incorporating Life Cycle Assessments into Building Project Decision Making: An Energy Consumption and CO2 Emission Perspective. Energy 2011, 36, 3022–3029. [Google Scholar] [CrossRef]

- Maximum Problem Dimensions. Available online: http://www.lindo.com/doc/online_help/lingo15_0/maximum_problem_dimensions.htm (accessed on 26 November 2016).

| Panel A: Production Information | Process 0 | Process 1 | Process 2 | ||||

| Product D10 | Product D20 | Product D30 | Product D11 | Product D21 | |||

| Maximum demand | Ri0 | Ri1 | 8000 | 9000 | 6000 | 4800 | 4000 |

| Selling price | Xi0 | Xi1 | $145 | $144 | $135 | $155 | $155 |

| Production Coefficient | ei | fi | 1 | 1 | 1 | 1 | 1 |

| Material of APIs | MA0 | MAi1 | $70 | $20 | $25 | ||

| Labor hours | tli0 | tli1 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 |

| Machine hours | tmi0 | tmi1 | 0.7 | 0.6 | 0.5 | 0.4 | 0.3 |

| Setup hours | tbi0 | tbi1 | 2 | 3 | 5 | 2 | 2 |

| Inspection hours | tτi0 | tτi1 | 100 | 100 | 150 | 300 | 250 |

| VOC disposal hours (per batch) | 10 | 50 | 45 | ||||

| Quantity of batch | bi0 | bi1 | 560 | 560 | 300 | 180 | 180 |

| Quantity of shipment | si0 | si1 | 280 | 280 | 150 | 90 | 90 |

| Carbon Tax Constraint | |||||||

| Carbon tax rate: m1 = $3/unit; m2 = $4/unit; m3 = $5/unit | |||||||

| The upper limit of three carbon emission charge level: Q1 = 12,000; Q2 = 15,000; Q3 = 25,000 | 3 | 2 | 2 | ||||

| Marketing, plant guard and management | $400,000 | ||||||

| Panel B: Resources Consumed | Tableting Labor | Tableting Machinery | Ordering | Shipping | Inspection | VOC’s Disposal | |

| Resources | $717,640 | $430,440 | $10,000 | $123,000 | $70,250 | $105,000 | |

| Available capacity (hours) | = 18,640 | = 16,880 | = 250 | = 4100 | = 1000 | = 3000 | |

| Per hour/rate | kl = $38.5/h | km = $25.5/h | ko = $40/h | kδ = $30/h | kτ = $70.25/h | kv = $35/h | |

| Panel A: Quantity of Products Sold | TDABC | TOC | ABC | ||||

| Product D10 | 7840 | 7840 | 7840 | ||||

| Product D20 | 8960 | 8400 | 8960 | ||||

| Product D30 | 5400 | 6000 | 2400 | ||||

| Product D11 | 4500 | 4680 | 4680 | ||||

| Product D21 | 3960 | 3960 | 3960 | ||||

| Panel B: Resources Consumed | TDABC | TOC | ABC | ||||

| Capacity (h) | Consumed | Consumed | Consumed | ||||

| (h) | (%) | (h) | (%) | (h) | (%) | ||

| Tableting labor | 18,640 | 14,368 | 77.08 | 14,561 | 78.12 | 12,928 | 69.36 |

| Tableting machinery | 16,880 | 16,812 | 99.60 | 16,857 | 99.86 | 15,336 | 90.85 |

| Ordering | 250 | 101 | 40.40 | 104 | 41.60 | 89 | 35.60 |

| Inspection | 1000 | 900 | 90.00 | 900 | 90.00 | 900 | 90.00 |

| Shipping | 4100 | 3193 | 77.88 | 3217 | 78.46 | 2898 | 70.68 |

| VOC’s disposal | 3000 | 2400 | 80.00 | 2440 | 81.33 | 2450 | 81.67 |

| Panel C: Profit | TDABC | TOC | ABC | ||||

| Revenue | $4,499,000 | $4,524,400 | $4,152,800 | ||||

| Material costs | $2,335,200 | $2,354,200 | $2,141,400 | ||||

| Tableting labor | $553,168 | $560,599 | $497,728 | ||||

| Tableting machinery | $428,706 | $429,854 | $391,068 | ||||

| Ordering cost | $4040 | $4147 | $3547 | ||||

| Inspection cost | $63,225 | $63,225 | $63,225 | ||||

| Shipping cost | $95,780 | $96,520 | $86,960 | ||||

| VOC’s disposal cost | $84,000 | $85,400 | $85,750 | ||||

| Marketing, Plant guard & management | $400,000 | $400,000 | $400,000 | ||||

| Income based on resources used in production | $534,881 | $530,455 | $483,122 | ||||

| Unused capacity cost | $227,411 | $216,585 | $328,052 | ||||

| Income based on resources supplied to production | $307,470 | $313,870 | $155,070 | ||||

| Version | Total Variables | Integer Variables | Nonlinear Variables | Constraints |

|---|---|---|---|---|

| Super Lingo | 2000 | 200 | 200 | 1000 |

| Hyper Lingo | 8000 | 800 | 800 | 4000 |

| Industrial Lingo | 32,000 | 3200 | 3200 | 16,000 |

| Extended Lingo | Unlimited | Unlimited | Unlimited | Unlimited |

© 2016 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC-BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tsai, W.-H.; Chang, J.-C.; Hsieh, C.-L.; Tsaur, T.-S.; Wang, C.-W. Sustainability Concept in Decision-Making: Carbon Tax Consideration for Joint Product Mix Decision. Sustainability 2016, 8, 1232. https://doi.org/10.3390/su8121232

Tsai W-H, Chang J-C, Hsieh C-L, Tsaur T-S, Wang C-W. Sustainability Concept in Decision-Making: Carbon Tax Consideration for Joint Product Mix Decision. Sustainability. 2016; 8(12):1232. https://doi.org/10.3390/su8121232

Chicago/Turabian StyleTsai, Wen-Hsien, Jui-Chu Chang, Chu-Lun Hsieh, Tsen-Shu Tsaur, and Chung-Wei Wang. 2016. "Sustainability Concept in Decision-Making: Carbon Tax Consideration for Joint Product Mix Decision" Sustainability 8, no. 12: 1232. https://doi.org/10.3390/su8121232