Non-Financial Reporting—Standardization Options for SME Sector

Department of Finance, Banking and Accounting, Czestochowa University of Technology (CUT), ul. J.H. Dąbrowskiego 69, 42-201 Czestochowa, Poland

J. Risk Financial Manag. 2021, 14(9), 417; https://doi.org/10.3390/jrfm14090417

Submission received: 9 July 2021

/

Revised: 11 August 2021

/

Accepted: 13 August 2021

/

Published: 3 September 2021

(This article belongs to the Section Sustainability and Finance)

Abstract

:Non-financial reporting is the basic tool for presenting the implementation of sustainability goals (SDGs). This paper investigated the current status of non-financial reporting standardization in terms of small and medium-sized enterprises. The topic of non-financial reporting has been discussed in recent years from the perspective of large business entities. So far, it has only rarely been applied to SMEs. This will increase significantly in the coming years when such reports will also become obligatory for smaller entities. The first stage of the research, based on the method of analysis and criticism of the literature, will be prepared in the area of the subject taken, including relations between the main concepts: sustainability, non-financing reports, SMEs. The essential data source used for the article is reports published by the Global Reporting Initiative. Based on the research conducted, it can be concluded that it is necessary to develop non-financial reporting standards for SMEs. These results may become a valuable resource of knowledge and a set of samples that can be useful in developing this area. Especially since it can be expected that such reports will also be obligatory for SMEs.

1. Introduction

Further economic development of the world is possible only by preserving sustainability. It should be based on the process cycle in the environment. The term sustainability is the result of understanding the three aspects: social, environmental and economic taking into account the costs of current decisions for future generations. Sustainability is a contemporary and current issue that is recognized by scholars (Al-Ali et al. 2020) and is the main derivative of this concept for business. The communication of an organization’s performance in its economic, social and environmental dimensions to the parties concerned is the principal function of the CSR (Corporate Social Responsibility) reporting process. In this way, an enterprise demonstrates the effectiveness of its actions in the area of social responsibility management. Thus, the CSR reporting should be part of the process of creating an organization’s strategy, implementation of its action plans (Krištofik et al. 2016). Entrepreneurs should invest in CSR and seek to improve the quality of their relationships with their funders (Mastrangelo et al. 2019). Given the popularity of both sustainability and external reporting, it may come as no surprise that the conceptual joint venture of ‘sustainability reporting’ has become influential (Niemann and Hoppe 2018). Zyznarska-Dworczak concluded that the positive and normative theories in a complementary way enable a multifaceted analysis of factors impacting the corporate sustainability reporting development, and determining its scope and shape in the future (Zyznarska-Dworczak 2018).

Financial market regulators, stock exchanges and industry bodies are more active in issuing codes, guidance, standards, self-regulatory requirements and questionnaires. While there is a growing sophistication of the reporting improvisation in the type of information required, this is not accompanied by a significant trend in the venues for disclosure. What is clear is that there is a high demand for quality data, a weakness to be addressed through closer collaboration between regulators, standard setters, professional associations and reporters (Amran et al. 2014). Financial statements focus on accounting for and reporting on past events. “Reporting the past” is considered a significant limitation by many users of reports, resulting in a persistent information gap (Adamek-Hyska et al. 2019). Increasingly, there is a vocalized demand on their part to “report the future”. The response to the indicated needs is an increasing interest in non-financial data and its reporting. Also, this sphere of reporting is subject to increasingly detailed legal regulations, among others, concerning its obligatory nature and its relationship with traditional information presented in financial statements.

The non-financial data consist of descriptions, facts and opinions that are difficult to express in a monetary measure or that are expressed in a non-monetary measure (Gernon and Meek 2000). They can be of retrospective or prospective nature. They are becoming a significant element of reporting of numerous entities. In the past, non-financial reporting was only a good practice in enterprises. In order to increase consistency and comparability of non-financial information shown in the territory of the Union, some large entities should prepare a statement on non-financial data containing information on environmental, social and labor issues, respect for human rights, counteracting corruption and bribery (Directive No. 2014/95/EU). This regulation concerns approximately 6000 large entities functioning within the EU area. The European Commission plans to extend the non-financial reporting obligation, currently required of large entities, to small and medium-sized enterprises as well.

Micro, small and medium-sized enterprises (SMEs) constitute 99% of the companies in the contemporary market economy. They provide two-thirds of private-sector jobs and contribute to more than half of the total added value created by businesses in the EU. Their operation is of great significance to owners, employees, local communities and primarily—the macro-economic growth of the country. SMEs should be treated as the main element of the global economy (Rittenhofer 2015). The problems and challenges they face are most frequently resolved intuitively, with the practice of operation of SMEs only using the achievements of management sciences to a rather minor extent. The recent years have resulted in an intensification of discourse concerning the development of the SME sector. This issue has been the subject of scientific analyses in various fields and dimensions. It itself proves that SMEs are of enormous significance for the operation of the contemporary economic market (Ali Qalati et al. 2020).

Many of those managing SMEs do not have formal, scientific knowledge in terms of financial management, which is necessary to conduct balanced economic activity. The specifics of the operations of SMEs should be taken into account when designing management mechanisms. The non-financing report is not to be solely reserved for large economic entities. It does, however, require adaptation to the size of the entity due to the limited scope (Ruzzier et al. 2015).

The term “socially responsible enterprise” is not reserved only for large business entities. Regardless of company size, CSR values matter (Baumann-Pauly et al. 2013), and SMEs may benefit from being socially responsible. Small and medium-sized enterprises are also able to meet the challenge of sustainability goals (SDGs) Most importantly, the implementation of CSR is not directly a function of company size. Non-financial reports have become an important tool in CSR management. The study aims to investigate the standardization of non-financial reporting in the case of the SME sector. It assesses the regulatory landscape of non-financial reporting as a management tool of sustainability.

The first stage of the research is based on the method of analysis and criticism of the literature. This stage is auxiliary and constitutes a starting point for further research. Quantitative methods are used to analyze the data. The study is based on historical sources. The study uses statistical data published by: GRI Database. The Global Reporting Initiative (GRI) is the most commonly used of those frameworks and has produced several generations of guidelines (Simmons et al. 2018). Interpretation based on the available literature on the subject and the analysis of reports will help to draw a picture of non-financial reporting from the perspective of SMEs.

The article is divided into the following sections: introduction, the review of the literature, materials and methods results, discussion, conclusions and references. The section on results includes standardization options for non-financing reporting, non-financial reporting depending on the size of the entity. The conclusions and discussion sections indicate the most important results and further research topics.

2. The Review of the Literature

It has been almost four decades since environmental disclosure has been an area of interest and attention for academic researchers (Elgobbi et al. 2020). Similarly, the problem of scarcity has been discussed for many years. It can be defined as the basic economic problem of people having limited resources with a simultaneous increase in demand for individual goods. Customers pay attention to these issues while making decisions (Ingaldi et al. 2021). Recently, stakeholders have demanded that reporting of a company provide social and environmental information as well as the financial information reported in the financial statement (Panggabean et al. 2014). Corporate social responsibility has now been widely accepted as an essential issue for corporations (Bidari and Djajadikerta 2020). It is also important to remember the limitations of the concept itself. The central aspect of transparency is balance, which means both positive and negative disclosure. Firms are expected to be transparent about the impacts and outcomes of their CSR, but are they (Einwiller and Carroll 2020)?

A sustainability report is an organizational report that gives information about the economic, environmental, social and governance performance. In other words, sustainability reporting is the practice of measuring, disclosing and being accountable to internal and external stakeholders for the company’s ability to achieve sustainable development goals and manage impacts on society (Calabrese et al. 2017). Providing stakeholders with information about the organization’s activities in its economic, social and environmental dimensions is the main function of the CSR (Corporate Social Responsibility) reporting process. In this way, the enterprise demonstrates the effectiveness of its actions in the area of social responsibility management. CSR reporting should be a part of the process of creating the organization’s strategy and implementing its action plans (Krištofik et al. 2016; Piersiala and Grabińska 2018).

Non-financial reporting at the national level is being researched by many scientists. Caesaria and Basuki analyzed the situation of Indonesia. They concluded that economic, environmental, and social aspects have a positive significant influence on the market performance of entities (Caesaria and Basuki 2017). Truant, Corazza and Scagnelli tested the relationship between a large Italian organization’s level of risk disclosure and other relevant variables (Truant et al. 2017). Woźniak and Pactwa compared the value of revenues to the budgets of local government units (communes) to the operating fee paid by entrepreneurs and expenditures of these municipalities on environmental protection, as the additional support by these entities in Poland (Woźniak and Pactwa 2017).

The limits of financial disclosure in fulfilling the investors’ needs have led to the request for reporting frameworks, capable of incorporating information of different natures. Integrated reporting (IR), which is the latest novelty in the organizational reporting practice, promises to gather the material on the financial and non-financial information (Frost n.d.; Stubbs and Higgins 2018; García-Sánchez et al. 2020).

Small-sized enterprises, very often constitute the backbone of the economy (Niciejewska and Kiriliuk 2020). Maj, Hawrysz and Bębenek verified whether selected variables, that is: the size of the company, the issue of operating on foreign markets and the financial performance influence the detail of the disclosed non-financial information (Maj et al. 2018). Their analysis has shown, that only in a few cases a statistically relevant dependency between analyzed variables exists, that is, between the size of the company and the disclosure of social and employee-related information towards internal stakeholders, between operating on foreign markets and the disclosure of social and the employee-related information towards external stakeholders, between the financial performance of the organization and respect for human rights, anti-corruption and bribery matters as well as the employee diversity.

Over the last decade, the confidence in reliable financial information has been significantly dented, which has largely influenced the change in the EU arrangements for the disclosure of non-financial matters (Wójcik-Jurkiewicz and Emerling 2020). At present, the topic of non-financial reporting is studied and described by many researchers and their conclusions are widely published. Obłoz presented the evaluation of the development of non-financial reporting in Poland before the EU Directive 2014/95/EU took effect in 2017. The analysis of non-financial companies’ reports led by the author, who so far had published the information and non-financial results freely, allowed to define market trends and good reporting practices in the Polish market (Obloza 2018).

The disclosure of the non-financial information by stock-exchange-listed companies in Poland, in the light of the changes introduced by the Directive 2014/95/EU is described by Szadziewska, Spigarska and Majerowska. Results of their research on non-financial reporting encompass the last reporting period prior to the introduction of the changes to the Act on Accounting. Their paper presents the results of an analysis of corporate non-financial disclosures in Poland within five sectors, that is, food, paper and wood products (furniture), chemical, energy and construction (Szadziewska et al. 2018).

While company size does not by definition determine the CSR implementation approach, the size implies a range of organizational characteristics, some of which are more, others less, advantageous for implementing CSR (Baumann-Pauly et al. 2013). Socially responsible business and ethical behavior of companies have been of interest to academia and practice for decades. However, the focus has almost exclusively been put on large corporations, while small- and medium-sized enterprises (SME) have not received as much attention (Hammann et al. 2009). In a financial economic scenario, in which the corporate survival of small and medium enterprises (SMEs) is more conditioned than ever with the competitive performance, this article aims to show that the strategic incorporation of socially responsible actions, more concerned and engaged with stakeholders, contributes to improving the competitiveness of these organizations (Herrera Madueño et al. 2016). Spanish and Peruvian examples show that the values of the owners and managers direct the policies of CSR. In some cases, the demands of employees and consumers are satisfied with obtaining benefits; however, in other cases, those demands are satisfied with a non-instrumental approach (Moneva and Hernández-Pajares 2018).

The limits of the financial disclosure in meeting the investors’ needs have led to the request for reporting frameworks capable of incorporating information of different natures. Integrated reporting (IR), which is the latest novelty in organizational reporting practice, promises to bring together material financial and non-financial information (Raimo et al. 2021). Entrepreneurs must skillfully use available information and resources in such a manner that ensures their company’s survival, development and competitiveness in the market. Therefore, it is up to the entities to decide whether to supplement the established information scope of the financial statements with disclosures that are important for the implementation of principles for a true and faithful picture of their entity (Chluska 2016).

SMEs, despite being able to adapt to the changing environment more effectively and faster than large business entities, are exposed to a number of difficulties (Kokot-Stępień and Krawczyk 2017). They often face difficulties in accessing capital, external funding sources, also information and infrastructure, as well as modern technologies and innovations, especially in the early stages of development. The management of small- and medium-sized enterprises is characterized by certain specificities that distinguish it from the management of large economic entities. This is pointed out by authors of numerous publications in this field (Brendzel-Skowera 2021; Chandra et al. 2020; Kiełtyka and Smoląg 2015; Kuraś 2020; Rudawska 2018; Ciekanowski and Wyrębek 2020). They do not use tools useful for management, which limits their development. Development issues are relegated to the background, giving way to current issues (Waśniewski 2014). Cluster Management Organization CMO can support SMEs, through joint action initiatives, in their transitions towards identifying sustainability-related objectives and in the adoption of hands-on and actionable management tools (Jiménez et al. 2021). Adapting the selected tools to their specifics, may increase the quality of the management.

In 2018, The European Federation of Accountants and Auditors for SMEs (EFAA) published the results of a survey from 14 European Countries. The EFAA suggested that the following policy considerations should be taken into account for further discussion:

- -

- SMEs should be encouraged to consider voluntarily providing NFI as this may yield benefits to them, their stakeholders and the wider public;

- -

- Some elements of the Non-Financial Reporting Directive (NFRD) might be suitable for voluntary adoption by SMEs;

- -

- National regulators should be encouraged to refer to the NFRD if formulating NFI requirements for their SMEs as this will help enhance the international comparability of NFI reporting by SMEs.

Legal aspects of non-financial reporting requirements for small and medium-sized enterprises do not exist. The EU law requires large companies to disclose certain information on the way they operate and manage social and environmental challenges. This practice helps investors, consumers, policymakers and other stakeholders to evaluate the non-financial performance of large companies and encourages these companies to develop a responsible approach to business. Directive 2014/95/EU—also called the non-financial reporting directive (NFRD)—lays down the rules on disclosure of non-financial and diversity information by large companies. This directive amends the accounting directive 2013/34/EU. Companies are required to include non-financial statements in their annual reports from 2018 onwards. EU rules on non-financial reporting only apply to large public-interest companies with more than 500 employees. This covers approximately 6000 large companies and groups across the EU, including: listed companies, banks, insurance companies and other companies designated by national authorities as public-interest entities. The European Commission plans to extend the obligation of non-financial reporting, to which large entities are currently obliged, also to small and medium-sized enterprises. Extensive consultations are currently being carried out in this regard.

Due to the possibility of the emergence of a legal obligation of non-financial reporting for small and medium-sized enterprises, further increases in CSR-related reporting can be forecasted. The growing level of non-financial reporting among SMEs and, at the same time, the growing trend of enterprises not using any of the GRI indicates the need to create a standard dedicated to this particular group of entities.

A significant challenge for entities preparing various regulations and standards is to create an attractive offer of products dedicated to enterprises from the SME sector. The situation is similar when it comes to CSR reporting. As research shows, micro, small and medium enterprises still rarely (although increasingly often) prepare non-financial reports. It is worth constructing such an offer to enable small and medium companies to implement ambitious management processes, including the use of CSR.

The research carried out by the Academy for the Development of Philanthropy showed that owners of small companies do a lot of what we call responsible business, not knowing the conceptual apparatus assigned to CSR (EFAA 2018). They are motivated by recognition in the local environment. It worked on the principle: I am an employer and I want to be a good neighbor, a good boss. Ownership reputation was a very important element in building human teams. Also, supporting local communities, or community involvement. These are the pillars of local CSR in SMEs. Intuitive action has its advantages and is particularly valuable for companies. Developing financial reporting standards, taking into account the specifics of SME operation, will raise awareness and give tools for more effective management using CSR. These standards may be all the more necessary as the European Commission is consulting on extending the reporting obligation to small and medium-sized entities.

The literature on the subject and many national and international reports intensively address the issue of constraints on SME growth due to funding gaps. The expansion requires a supply of funds, which may be of various origins, own and foreign, domestic and foreign, public and private, repayable and non-repayable, etc. In order to access each of these, it is important to present the enterprise in the best possible light. A financial report is a synthetic picture of a company, but it is worth extending it with information on CSR.

The topic of the study as well as the analysis of literature and industry reports point to the following research questions:

- -

- Q1: What are non-financial reporting obligations for small and medium-sized enterprises?

- -

- Q2: What are the options for standardizing non-financial reporting for small and medium-sized enterprises?

- -

- Q3: What are the needs of small and medium-sized enterprises in the area of standardization of non-financial reporting?

3. Materials and Methods

The study is based on historical sources. The study uses statistical data published by: GRI Database. Publications developed by this institution are highly reliable, and thus, the collected research material is credible. It is the best known and most widely used document to aid the preparation of non-financial reports for organizations around the world (Czaja-Cieszyńska 2018). Its strategic partners include the Organization for Economic Cooperation and Development (OECD Guidelines for Multinational Enterprises), the United Nations (Global Compact and Communication on Progress) or the International Organization for Standardization (ISO 26000, International Standard for Social Responsibility). It is easier for organizations to communicate their efforts to support the UN Sustainable Development Goals (SDGs), by using the most widely adopted standards for sustainability reporting—the GRI Standards.

The organization also collects non-financial reports from all around the world in its database. The GRI Sustainability Disclosure Database is a publicly available online repository of sustainability reports, both GRI and non-GRI based. This database includes thousands of reports published since 1999. It allows the user to search for reports by several criteria including: size (see Table 1), sector, country, region, report type, report year. Thanks to such an advanced filtering system for GRI search engine reports, it was possible to select the data subject to further analysis. From the perspective of the study, the most important criteria will be the breakdown by the entity size and the year of publication of the report.

The study covered the period from 1999–2020. At the time of the survey, the GRI database contained 63,744 reports. For the purposes of this study, three filters were used:

- -

- Size,

- -

- Report type,

- -

- Report year.

The first group divided the reports into three groups: Large, MNE and SME. The quantitative criteria for this division are listed in Table 1. The field report type indicates the version of the GRI Guidelines applied in the report: GRI–G1 (published in 2000), GRI–G2 (published in 2002), GRI–G3 (published in 2006), GRI–G3.1 (published in 2011), GRI–G4 (published in 2013), GRI–Standards (published in 2016), Citing-GRI, No GRI. The last filter used relates to the time period 1999–2020. Due to the ongoing review of the database information on the GRI platform to avoid misinterpretation of data and trends, the Report Year filter is disabled for the years 2018, 2019 and 2020. The 2018–2020 period was treated in total and then the average values were calculated.

The detailed data on the use of standards by SME entities is presented. The data gathered from the GRI Database are presented in tables in numerical form. The percentage share depending on the size of the entity is calculated. The results of the study are also presented in the form of a chart.

4. Results

The question concerning the legal obligation of non-financial reporting for small and medium companies will be answered first. Then, the most frequently used options for standardizing non-financial reporting will be presented. The analysis of their usefulness from their point of view will be performed.

4.1. Standardization Options for Non-Financing Reporting

What are the prospects for the upward harmonization of regulatory standards, and why do governments support or oppose more stringent supranational regulation? Kinderman attempts to answer these questions (Kinderman 2020). There have been numerous initiatives that started to build the theoretical background behind the possible approaches to guide non-financial reporting. For that reason, various international organizations have been established (De 2020).

By imposing the obligation to prepare non-financial reports, the legislator allows entities to choose the way of preparing the report. Enterprises do not have a duty to use any formalized standards or guidelines. They are obliged only to refer to these issues assigned in the Directive and, as a consequence, the amended Accounting Act. The international business environment offers many standards, guidelines, and reporting frameworks that entities may adopt when preparing a non-financial report:

- -

- Global Reporting Initiative (GRI),

- -

- Standard of Non-Financial Information (SIN)

- -

- Communication on Progress (Global Compact),

- -

- International Integrated Reporting Framework,

- -

- Guidance on Corporate Responsibility Indicators in Annual Reports,

- -

- KPIs for ESG,

- -

- Model Guidance on Reporting ESG Information for Investors,

- -

- Reporting framework in line with the UN Guiding Principles on Business and Human Rights,

- -

- Carbon Disclosure Project,

- -

- Greenhouse Gas Protocol Corporate Standard,

- -

- Principles for Responsible Investment,

- -

- OECD guidelines for multinational enterprises,

- -

- PN-ISO 26000: 2012 regarding social responsibility and others.

Taking into consideration the lack of strict legal regulations while so many opportunities, a good approach to the situation could be using one of the available norms, guidelines or standards. The report with the usage of these standards leads to more trust. It can be also decided on an indirect output: formally, neither reporting using any of the standards nor relying on any of them, that is, treating it as a support. There are many guideline options, but only some of them are described widely enough to allow reporting all of the aspects, which are directly shown in a law. Each of the methods and tools has its strong and weak points. There is not a single entirely good solution. All of the people who are reporting should be aware of one thing: no matter which standard or guidelines they are using, it is necessary to include in the report all elements referred to in the directive.

It is worth analyzing which of these standardization norms relate to the mandatory issues in the Directive (Directive 2014/95/EU of the European Parliament and of the Council), that is:

- -

- Environmental,

- -

- Social and labor rights,

- -

- Human rights,

- -

- Anti-corruption.

The following stage will address the applicability of the norm depending on the size of the company. In Table 2, a synthetic summary of selected standardization options is presented, taking into account the name, the entity developing the standard, the reporting areas covered. It is particularly important from the point of view of the subject matter, which entities it is dedicated to, and whether it can be used by SMEs.

According to authors of the rapport Carrot and Sticks from 2016, almost 30% of reporting instruments apply only to large listed companies and of these, almost three-quarters (73%) are from financial market regulators and stock exchanges. A further 14% of all instruments apply to large companies, both listed and unlisted. Around 40% of sustainability reporting instruments apply either to all companies (without distinction by size, listing or sector) or to all companies except for state-owned companies. Large companies in the public eye are arguably more likely to attract scrutiny for their sustainability performance than many smaller companies.

Despite this, small and medium enterprises (SMEs) play a critical role in global value chains because large companies often rely on them to supply raw materials, goods and services. There is therefore an ongoing debate around whether SMEs should account for their sustainability impacts in the same way as most large companies do. Policymakers face a dilemma here. SMEs have limited resources to report so voluntary instruments may have limited impact. This leaves policymakers and regulators with the decision of whether or not to introduce instruments that mandate sustainability reporting by smaller companies.

Based on the information in Table 2, the following conclusions can be reached:

- -

- Ten standardization options of international relevance were analyzed, addressing mandatory issues (environmental, social and labor rights, human rights, anti-corruption) on which entities of all sizes and activities can rely.

- -

- Eight of the ten norms refer to all four mandatory areas of financial reporting (environmental, social and labor rights, human rights, anti-corruption). This means that they are mostly quite universal. The International Integrated Reporting Framework prepared by the International Integrated Reporting Council (IIRC) does not address the issue of corruption. In contrast, the Guidance on Corporate Responsibility Indicators in Annual Reports by UNCTAD developed by the United Nations Conference on Trade and Development omits environmental and human rights issues.

- -

- Among the addressees of the standards, we can find enterprises, government agencies, administrations, cities, social and educational organizations, employers’ organizations, trade unions. Most entities stress that standards can be applied regardless of size or sector.

- -

- Five of the ten standards can be applied regardless of the size of the entity. This means that half of them can also be applied to micro, small and medium-sized enterprises. The Communication on Progress developed by the UN Global Compact excludes entities with up to 10 employees, that is, in practice all micro entities. The KPIs for ESG of the European Federation of Financial Analysts Societies and the DVFA Society of Investment Professionals in Germany are specifically designed for stock market investors.

The presented information indicates that there is no option to standardize non-financial reports individually adapted to the specificity of SMEs.

4.2. Non-Financial Reporting Depending on the Size of the Entity

The essence of the social responsibility reporting process is contained in the selection of properly presented non-financial data and the manner of their presentation (Piłacik 2019). A consistent framework for social responsibility reporting is the Global Reporting Initiative (GRI) guidelines developed by a non-profit association, whose activities are based on the cooperation of a network of stakeholders and the support is being received from the United Nations Environment Programme.

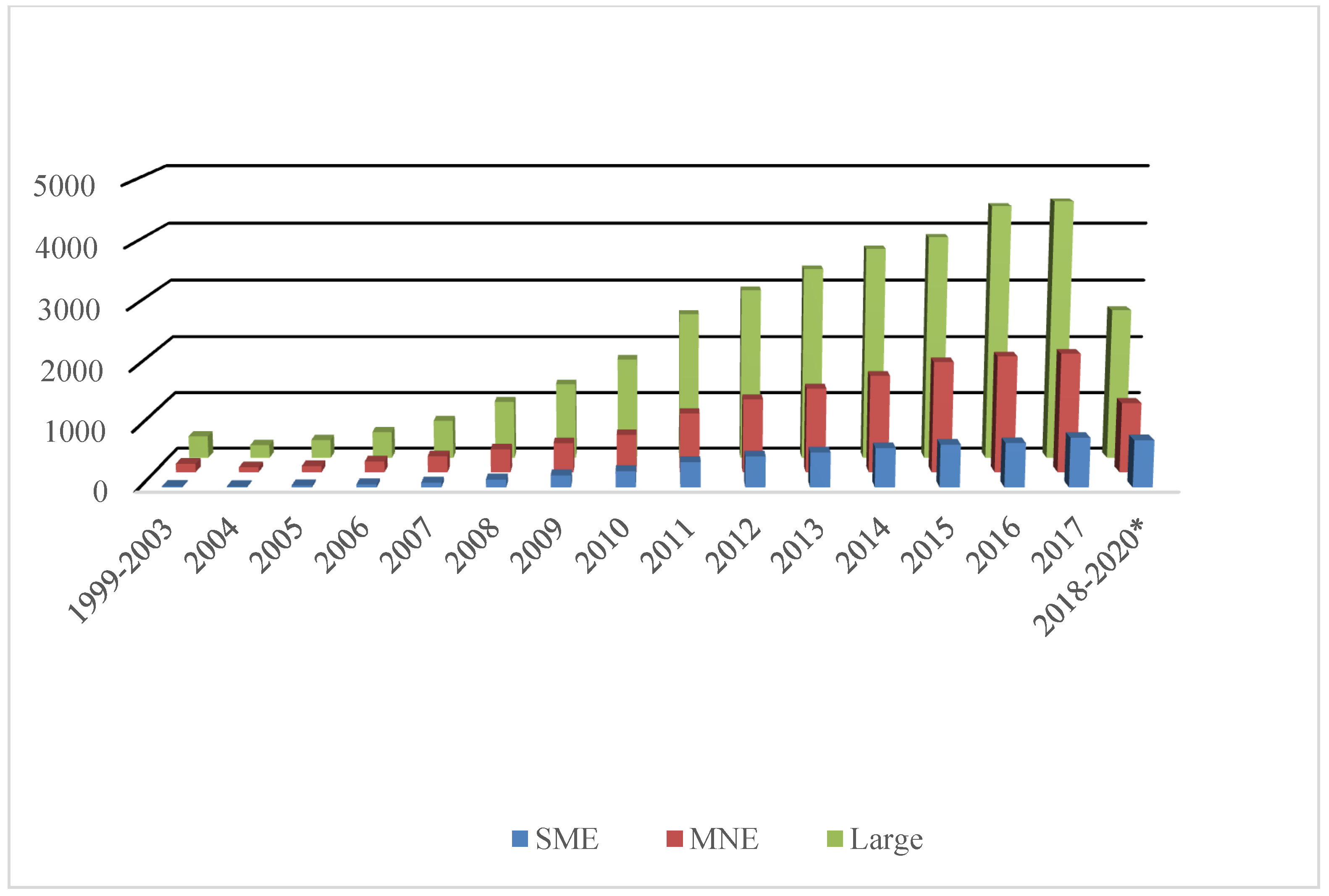

Table 3 and Figure 1 show the level of development of non-financial reporting in the period from 1999 to 2020. The calculations presented, based on data taken from GRI, allow the following conclusions to be drawn:

- -

- The level of non-financial reporting is steadily increasing. Each year brings an increase in the number of reports. The largest quantitative increase took place in 2011, with 1310 reports (2011—3960 reports, 2010—2650 reports). The largest percentage increase in the number of reports was achieved in 2006, by almost 55% (2005—446 reports, 2006—688 reports).

- -

- Regardless of the size of the company, the number of reports increased every year. During the period in question, there was a significant predominance of reports prepared by large entities—61.07%, with reports prepared by large international entities (MNEs) accounting for 26.9% and small and medium-sized entities accounting for 12.03%.

- -

- It is important to highlight the clearly discernible trend of increasing the level of reporting among small and medium-sized entities. Their share in the total number of reports in the over 20-year period under review increased from 3.5% to 17.33%. The average for the period was 12.03%.

- -

- The share of large international (MNE) reporting has fluctuated over the period studied. It was highest in 2015 at 29.24% and lowest in 2005 at 23.32%.

- -

- The share of reports of the largest entities decreased from almost 70% in the first years to a level of 56.69% in 2018–2020.

- -

- Taking into account the share, the importance of non-financial reports of small and medium-sized entities is increasing with an overall increase in the number of reports. This means that this sort of report is of significance also for small entities, despite the absence of a legal obligation to prepare reports.

The analysis of the information presented in Table 4 allows several essential conclusions to be reached:

- -

- The detailed analysis of individual years and selected standardization options shows that SMEs strive to use the latest recommended standards. In the last analyzed period between 2018–2020, they most often use GRI Standards. More than 50% of all reports in the database during this period were developed with the usage of this standard.

- -

- Throughout the 1999–2020 period, GRI–G3 was used most frequently. GRI–G1 (0.12%) and GRI–G2 (1.19%) were the least frequently used, in the early years the use of these standards was high.

- -

- It is disturbing the increasing values in the NO GRI column. In the first period, 4 out of 19 reports (~20%) did not use GRI. In 2017, the value was the highest—455 out of 833 reports (almost 55%). Looking at the average for the whole period 1999–2020, it can be concluded that one-third of the reports did not rely on any of the GRI standards.

- -

- Once again, the increase in the number of non-financial reports among SMEs can be confirmed. This confirms the growing importance of reports as an element of business management.

5. Discussion

The results of the conducted analyses allow answering the research questions raised:

- -

- What are non-financial reporting obligations for small and medium-sized enterprises?

- -

- What are the options for standardizing non-financial reporting for small and medium-sized enterprises?

- -

- What are the needs of small and medium-sized enterprises in the area of standardization of non-financial reporting?

Currently, there is no legal obligation for small and medium-sized entities to report non-financial information. However, this legal status may change due to two reasons. The first of these is the growing importance of non-financial reports in making economic decisions. Traditional financial reports, which were supposed to be of objective nature due to their synthetic features, are found to be insufficient. Secondly, in Europe, and indeed in many if not most other regions, small and medium-sized enterprises account for the majority of private-sector GDP, employment and environmental and social impact. It is perhaps no surprise then that some wonder whether SMEs should disclose such impacts. The European Commission is considering the extension of the non-financial reporting obligation for SMEs. Extensive consultations are currently taking place in this regard.

International business organizations offer many norms and standards that can improve the quality of non-financial reporting. Many of them refer to all four most important areas (environmental, social and labor rights, human rights, anti-corruption). However, there is no standard that takes into account the specificities of SMEs. Taking into account the growing interest in non-financial reporting and the importance of SMEs and their unique character, there is a need to create standardization norms for these entities, similarly to many other procedures in areas of management.

Accounting is more than a technical methodology for accumulating data of financial position and performance (Atkins et al. 2018). It has the potential to encourage change at the social, organizational and individual levels. Accounting systems, and the information they produce, are thus assumed to facilitate accountability, the giving and demanding of reasons for conduct (Du Rietz 2018). Accountants need to know that any accounting information is flawed, it highlights certain issues and conceals others, it does not question that information facilitates the demand for accountability and enables control. The same is true of non-financial information, it should be as unbiased, fair and factual as possible. Reporting standards go a long way toward making data more objective. However, they do not provide 100% assurance on the impartiality of the information. Nevertheless, it is important to study the non-financial information that they provide because disclosure of nonfinancial information is a way to improve companies’ transparency and communication of social and ethical practices.

The non-financial statement ceases to be voluntary and becomes a legal obligation for many companies. Legislators leave entities free to choose their reporting standards, and the standard formulas often allow for a fair amount of autonomy in choosing what is to be included in the report. There is not always a legal obligation for external integrity verification similar to that performed by auditors for financial reports. Thus, for non-financial reports, which are used to communicate with stakeholders, companies choose at their own discretion the data they consider relevant. It is to be trusted by stakeholders that the information is reliable and of essence from the stakeholders’ standpoint.

6. Conclusions

Today’s accounting cannot be limited to a synthetic numerical description of business management. It must take into account reporting sustainability goals (SDGs). The traditional approach to accounting that reduces it to a field of science conflicts with the idea of non-financial reporting. The redefinition of the financial reporting model as well as changes in its structure and scope are driven by the changing information needs of financial reports users (Śnieżek et al. 2018). They want to make decisions based on financial and asset information from traditional financial statements, information about adopted strategies. The impact on the socio-economic environment is also deemed important to them.

Non-financial reporting is a toll on sustainability. It is also a form of transparency reporting where businesses formally disclose certain information not related to their finances, including information on human rights, environmental, social and labor rights, and anti-corruption. It helps organizations to measure, understand and communicate impacts of those areas, as well as set goals, and manage change more effectively.

The concepts, according to which organizations at the stage of strategy building take into account social interests and environmental protection as well as relations with other entities, have already existed for two decades. Combining these two elements resulted in creating non-financial reports. The research in this field intensified the introduction of Directive 2014/95/EU. Obligatory reporting of non-financial entities by selected entities occurred for the reports for 2017. This is a breakthrough moment for the social side of business. SMEs are currently excluded from the NFRD, although those in the supply chain of larger companies may already be dealing with demands for more non-financial information. Such SMEs would likely be aware of the impact of future changes to the scope of legislation.

Different studies indicate that SMEs can found benefits in their CSR performance. Being a socially responsible entity is a sign of prestige. Companies, for which CSR values matter, far more quickly observed that the fact of being socially responsible is worthbeing presented. An essential tool in this process became social reports. The reporting period for 2017 turned out to be a breakthrough. Before the EU Directive 2014/95/EU appeared, in some countries, there was already an obligation to report non-financial data. It can be noted that CSR communication practice is heading for new shores. Economic pressure, legal and political requirements, reputation risks in the digital media and well-being-oriented generation of employees (Weder et al. 2019). The concept of communication responsibility as a normative framework for corporate communication is evolving. In preparing for further discussion, it is imperative to take into account SME entities, which have been wrongly left out of the CSR discussion.

As usual, this investigation may have a number of potential shortcomings restricting its validity. One is the clear focus on regulations stemming from the European legal mainstream. The second limitation results from the GRI Database. Due to the ongoing review of their database and its related registration process, the information on this platform was last updated in December 2020 and is not going to be further populated. In order to avoid misinterpretation of data and trends, the Report Year filter is disabled for the years 2018, 2019 and 2020, due to a partial upload of data related to that period. The reports available in the database for 2018–2020 are still searchable through other filters. Despite the limitations introduced in the GRI search engine, research material was collected for the period 1999–2020. Therefore, it is the reason for this period being treated as a whole and it could not be separated into individual years in Table 3 and Table 4.

The purpose of this article was to investigate the area of non-financial reporting standardization in terms of the specificity of small and medium-sized enterprises. The method of literature analysis in terms of SMEs and nonfinancial information of enterprises as well as report analysis and own observations was used. The article answers the research questions raised in a comprehensive manner. However, the topic remains interesting and will certainly be discussed further at the levels of academic discussion, international organizations and business practice. The original and new contribution of the study is a combination of two popular topics: non-financial reporting and SMEs in one topic.

So far, there is no obligation for small and medium-sized entities to report non-financial information, but this may change in the near future. The interest of small and medium-sized enterprises in non-financial reporting is growing. Based on the research conducted, it can be concluded that it is necessary to develop non-financial reporting standards for SMEs. The presented topic should be monitored in the future. Changes in legal regulations in this area and their impact on the behavior of enterprises should be checked, especially if non-financial reporting becomes obligatory for small and medium-sized enterprises. Will legal obligation result in the creation of a standard dedicated to SMEs?

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Publicly available datasets were analyzed in this study. This data can be found here: https://database.globalreporting.org/.

Conflicts of Interest

The author declares no conflict of interest.

References

- Adamek-Hyska, Dorota, Katarzyna Tkocz-Wolny, Marzena Strojek-Filus, and Aneta Wszelaki. 2019. Zmiany Zakresu Informacyjnego Raportów Finansowych i Niefinansowych. Warszawa: Księgarnia Internetowa PWN. [Google Scholar]

- Al-Ali, Mubarak Noor Y. M., Eva Gorgenyi-Hegyes, and Maria Fekete-Farkas. 2020. Perceived corporate sustainability practices and performance of small and medium enterprises (smes) in qatar. Polish Journal of Management Studies 22: 26–42. [Google Scholar] [CrossRef]

- Ali Qalati, Sikandar, Wenyuan Li, Naveed Ahmed, Manzoor Ali Mirani, and Asadullah Khan. 2020. Examining the Factors Affecting SME Performance: The Mediating Role of Social Media Adoption. Sustainability 13: 75. [Google Scholar] [CrossRef]

- Amran, Azlan, Shiau Ping Lee, and S. Susela Devi. 2014. The Influence of Governance Structure and Strategic Corporate Social Responsibility Toward Sustainability Reporting Quality—Amran—2014—Business Strategy and the Environment—Wiley Online Library. Available online: https://onlinelibrary.wiley.com/doi/abs/10.1002/bse.1767 (accessed on 10 November 2020).

- Atkins, Jill, Warren Maroun, Barry Colin Atkins, and Elisabetta Barone. 2018. From the Big Five to the Big Four? Exploring Extinction Accounting for the Rhinoceros. Accounting, Auditing & Accountability Journal 31: 674–702. [Google Scholar] [CrossRef]

- Baumann-Pauly, Dorothée, Christopher Wickert, Laura J. Spence, and Andreas Georg Scherer. 2013. Organizing Corporate Social Responsibility in Small and Large Firms: Size Matters. Journal of Business Ethics 115: 693–705. [Google Scholar] [CrossRef] [Green Version]

- Bidari, Gopi, and Hadrian Geri Djajadikerta. 2020. Factors Influencing Corporate Social Responsibility Disclosures in Nepalese Banks. Asian Journal of Accounting Research 5: 209–24. [Google Scholar] [CrossRef]

- Brendzel-Skowera, Katarzyna. 2021. Circular Economy Business Models in the SME Sector. Sustainability 13: 7059. [Google Scholar] [CrossRef]

- Caesaria, Aisyah Farisa, and B. Basuki. 2017. The Study of Sustainability Report Disclosure Aspects and Their Impact on the Companies’ Performance. SHS Web of Conferences 34: 08001. [Google Scholar] [CrossRef] [Green Version]

- Calabrese, Armando, Roberta Costa, Nathan Levialdi Ghiron, and Tamara Menichini. 2017. Materiality analysis in sustainability reporting: A method for making it work in practice. European Journal of Sustainable Development 6: 439. [Google Scholar] [CrossRef]

- Chandra, Ashna, Justin Paul, and Meena Chavan. 2020. Internationalization Barriers of SMEs from Developing Countries: A Review and Research Agenda. International Journal of Entrepreneurial Behavior & Research 26: 1281–310. [Google Scholar] [CrossRef]

- Chluska, Jolanta. 2016. Uproszczenia rachunkowości jednostek mikro i małych—Szanse i zagrożenia. Studia Ekonomiczne/Uniwersytet Ekonomiczny w Katowicach 268: 64–73. [Google Scholar]

- Ciekanowski, Zbigniew, and Henryk Wyrębek. 2020. Impact of micro, small and medium-sized enterprises on economic security. Polish Journal of Management Studies 22: 86–102. [Google Scholar] [CrossRef]

- Czaja-Cieszyńska, Hanna. 2018. Standardy GRI—Kierunek dla raportowania na rzecz zrównoważonego rozwoju w organizacjach pozarządowych w Polsce. Studia i Prace Kolegium Zarządzania i Finansów 164: 49–61. [Google Scholar]

- De, Luca Francesco. 2020. Prelims. In Mandatory and Discretional Non-Financial Disclosure after the European Directive 2014/95/EU. Bingley: Emerald Publishing Limited. [Google Scholar] [CrossRef]

- Du Rietz, Sabina. 2018. Information vs. Knowledge: Corporate Accountability in Environmental, Social, and Governance Issues. Accounting, Auditing & Accountability Journal 31: 586–607. [Google Scholar] [CrossRef] [Green Version]

- EFAA. 2018. Survey of Non-Financial Reporting Requirements for SMEs in Europe. Brussels: The European Federation of Accountants and Auditors for SMEs (“EFAA”). [Google Scholar]

- EFFAS. n.d. Available online: www.effas-esg.com (accessed on 10 November 2020).

- Einwiller, Sabine A., and Craig E. Carroll. 2020. Negative Disclosures in Corporate Social Responsibility Reporting. Corporate Communications: An International Journal 25: 319–37. [Google Scholar] [CrossRef]

- Elgobbi, Eltayeb, Mr Eltaib, E. El-Ghannai, and Assistant. 2020. The Impact of Quality Information on the Environmental Accounting Disclosure: A Case Study for the Arabian Gulf Oil Company in Libya. September. Available online: https://www.researchgate.net/publication/344237848_The_Impact_of_Quality_Information_on_the_Environmental_Accounting_Disclosure_A_Case_study_for_the_Arabian_Gulf_Oil_Company_in_Libya (accessed on 10 November 2020).

- Frost, Geoffrey. n.d. Integrating Sustainability Reporting into Management Practices. Accounting Forum. Available online: https://www.academia.edu/24571528/Integrating_sustainability_reporting_into_management_practices (accessed on 24 May 2021).

- García-Sánchez, Isabel-María, Nicola Raimo, Arcangelo Marrone, and Filippo Vitolla. 2020. How Does Integrated Reporting Change in Light of COVID-19? A Revisiting of the Content of the Integrated Reports. Sustainability 12: 7605. [Google Scholar] [CrossRef]

- Gernon, Helen, and Gary Kenneth Meek. 2000. Accounting: An International Perspective. Boston: McGraw-Hill. [Google Scholar]

- GRI. 2020. Sustainability Disclosure Database. Data Legend. Available online: https://www.globalreporting.org/media/m22dl3o0/gri-data-legend-sustainability-disclosure-database-profiling.pdf (accessed on 13 January 2021).

- GRI. n.d. Available online: www.globalreporting.org (accessed on 10 November 2020).

- Hammann, Eva-Maria, André Habisch, and Harald Pechlaner. 2009. Values That Create Value: Socially Responsible Business Practices in SMEs—Empirical Evidence from German Companies. Business Ethics: A European Review 18: 37–51. [Google Scholar] [CrossRef]

- Herrera Madueño, Jesús, Manuel Larrán Jorge, Isabel Martínez Conesa, and Domingo Martínez-Martínez. 2016. Relationship between Corporate Social Responsibility and Competitive Performance in Spanish SMEs: Empirical Evidence from a Stakeholders’ Perspective. BRQ Business Research Quarterly 19: 55–72. [Google Scholar] [CrossRef] [Green Version]

- Ingaldi, Manuela, Silvie Brozova, and Marina Zhuravskaya. 2021. Social Awareness and Responsibility in Context of Polish Service Companies. System Safety: Human—Technical Facility—Environment 3: 71–78. [Google Scholar] [CrossRef]

- Integrated Reporting. n.d. Available online: http://integratedreporting.org (accessed on 10 November 2020).

- Jiménez, Eduardo, Marta de la Cuesta-González, and Montserrat Boronat-Navarro. 2021. How Small and Medium-Sized Enterprises Can Uptake the Sustainable Development Goals through a Cluster Management Organization: A Case Study. Sustainability 13: 5939. [Google Scholar] [CrossRef]

- Kiełtyka, Leszek, and Klaudia Smoląg. 2015. Analysis of Business Intelligence Solutions in the SME Sectors. Applied Mechanics and Materials 795: 123–28. [Google Scholar] [CrossRef]

- Kinderman, Daniel. 2020. The Challenges of Upward Regulatory Harmonization: The Case of Sustainability Reporting in the European Union. Regulation & Governance 14: 674–97. [Google Scholar] [CrossRef]

- Kokot-Stępień, Patrycja, and Patrycja Krawczyk. 2017. Specyfika analizy finansowej w sektorze małych i średnich przedsiębiorstw. Marketing i Rynek 7: 367–76. [Google Scholar]

- Krištofik, Peter, Marzanna Lament, and Hussam Musa. 2016. The Reporting of Non-Financial Information and the Rationale for Its Standardisation. E+M Ekonomie a Management 19: 157–75. [Google Scholar] [CrossRef]

- Kuraś, Małgorzata. 2020. Corporate Social Responsibility as an Element of SME Management in Poland. International Business Information Management Association (IBIMA), pp. 15183–92. Available online: https://ibima.org/accepted-paper/corporate-social-responsibility-as-an-element-of-sme-management-in-poland/ (accessed on 10 November 2020).

- Maj, Jolanta, Liliana Hawrysz, and Piotr Bębenek. 2018. Determinants of Corporate Social Responsibility Disclosure in Polish Organisations. International Journal of Contemporary Management 17: 197–215. [Google Scholar] [CrossRef]

- Mastrangelo, Leonardo, Sonia Cruz-Ros, and Maria-Jose Miquel-Romero. 2019. Crowdfunding Success: The Role of Co-Creation, Feedback, and Corporate Social Responsibility. International Journal of Entrepreneurial Behavior & Research 26: 449–66. [Google Scholar] [CrossRef]

- Moneva, José M., and Julio Hernández-Pajares. 2018. Corporate Social Responsibility Performance and Sustainability Reporting in SMEs: An Analysis of Owner-Managers’ Perceptions. International Journal of Sustainable Economy 10: 405–20. [Google Scholar] [CrossRef]

- Niciejewska, Marta, and Olga Kiriliuk. 2020. Occupational Health and Safety Management in “Small Size” Enterprises, with Particular Emphasis on Hazards Identification. Production Engineering Archives 26. [Google Scholar] [CrossRef]

- Niemann, Ludger, and Thomas Hoppe. 2018. Sustainability Reporting by Local Governments: A Magic Tool? Lessons on Use and Usefulness from European Pioneers. Public Management Review 20: 201–23. [Google Scholar] [CrossRef]

- Obloza, Magdalena. 2018. Rozwój raportowania niefinansowego w Polsce przed wprowadzeniem wymogów dyrektywy 2014/95/UE. Marketing i Rynek 25: 322–36. [Google Scholar]

- Panggabean, Rosinta Ria, Nuraini Sari, Lidiyawati Lidiyawati, and Evi Steelyana. 2014. Corporate Social Reporting: A Comprehensive Picture of Indonesian Mining Companies. The Winners 15: 123. [Google Scholar] [CrossRef] [Green Version]

- Piersiala, Luiza, and Aleksandra Grabińska. 2018. Corporate Social Responsibility of Enterprises in Special Economic Zones in Poland. In Business Management and Corporate Social Responsibility (Red.) ŁĘGOWIK-ŚWIĄCIK Sylwia, SUROWIEC Anna. Ostrava: VSB—Technical University of Ostrava, pp. 119–28. [Google Scholar]

- Piłacik, Joanna. 2019. Raportowanie społecznej odpowiedzialności zgodnie z wytycznymi Global Reporting Initiative w krajach Unii Europejskiej. In Prace Naukowe. Katowice: Uniwersytet Ekonomiczny w Katowicach, pp. 86–96. [Google Scholar]

- PKN. n.d. Available online: http://www.pkn.pl/iso-26000 (accessed on 10 November 2020).

- PRI. n.d. Available online: www.unpri.org (accessed on 10 November 2020).

- Raimo, Nicola, Filippo Vitolla, Arcangelo Marrone, and Michele Rubino. 2021. Do Audit Committee Attributes Influence Integrated Reporting Quality? An Agency Theory Viewpoint. Business Strategy and the Environment 30: 522–34. [Google Scholar] [CrossRef]

- Rittenhofer, Iris. 2015. The Reflexive Case Study Method: A Practice Approach to SME Globalization. International Journal of Entrepreneurial Behavior & Research 21: 410–28. [Google Scholar] [CrossRef]

- Rudawska, Edyta, ed. 2018. Prelims. In The Sustainable Marketing Concept in European SMEs. Bingley: Emerald Publishing Limited. [Google Scholar] [CrossRef] [Green Version]

- Ruzzier, Maja Konecnik, Mitja Ruzzier, and Robert D. Hisrich. 2015. Marketing for Entrepreneurs and SMEs: A Global Perspective, reprint ed. Cheltenham: Edward Elgar Pub. [Google Scholar]

- Simmons, James Michael, Jr., Victoria L. Crittenden, and Bodo B. Schlegelmilch. 2018. The Global Reporting Initiative: Do Application Levels Matter? Social Responsibility Journal 14: 527–41. [Google Scholar] [CrossRef]

- SSE. n.d. Available online: www.sseinitiative.org (accessed on 10 November 2020).

- Stubbs, Wendy, and Colin Higgins. 2018. Stakeholders’ Perspectives on the Role of Regulatory Reform in Integrated Reporting. Journal of Business Ethics 147: 489–508. [Google Scholar] [CrossRef]

- Szadziewska, Arleta, Ewa Spigarska, and Ewa Majerowska. 2018. The Disclosure of Non-Financial Information by Stock-Exchange-Listed Companies in Poland, in the Light of the Changes Introduced by the Directive 2014/95/EU. Zeszyty Teoretyczne Rachunkowości 99: 65–95. [Google Scholar] [CrossRef]

- Śnieżek, Ewa, Joanna Krasodomska, Arleta Szadziewska, and GAB Doradztwo Wydawnicze Grzegorz Boguta. 2018. Informacje Niefinansowe w Sprawozdawczości Biznesowej Przedsiębiorstw. Warszawa: Wydawnictwo Nieoczywiste—Imprint GAB Media. [Google Scholar]

- Truant, Elisa, Laura Corazza, and Simone Scagnelli. 2017. Sustainability and Risk Disclosure: An Exploratory Study on Sustainability Reports. Sustainability 9: 636. [Google Scholar] [CrossRef] [Green Version]

- UN Global Compact. n.d. Available online: www.unglobalcompact.org (accessed on 10 November 2020).

- UN Guiding Principles. n.d. Available online: www.ungpreporting.org (accessed on 10 November 2020).

- UNCTAD. n.d. Available online: http://unctad.org (accessed on 10 November 2020).

- Waśniewski, Piotr. 2014. Pomiar wyników finansowych w małych i średnich przedsiębiorstwach. Zeszyty Naukowe Uniwersytetu Szczecińskiego. Finanse, Rynki Finansowe, Ubezpieczenia 66: 525–34. [Google Scholar]

- Weder, Franzisca, Sabine Einwiller, and Tobias Eberwein. 2019. Heading for New Shores: Impact Orientation of CSR Communication and the Need for Communicative Responsibility. Corporate Communications: An International Journal 24: 198–211. [Google Scholar] [CrossRef]

- Woźniak, Justyna, and Katarzyna Pactwa. 2017. Environmental Activity of Mining Industry Leaders in Poland in Line with the Principles of Sustainable Development. Sustainability 9: 1903. [Google Scholar] [CrossRef] [Green Version]

- Wójcik-Jurkiewicz, Magdalena, and Izabela Emerling. 2020. Ujawnianie Informacji Niefinansowych w Zakresie CSR. Dobre Praktyki. Katowice: Pub. Wydawnictwo UE of Katowice. [Google Scholar]

- Zyznarska-Dworczak, Beata. 2018. Accounting Theories towards Non-Financial Reporting. Studia Ekonomiczne/Uniwersytet Ekonomiczny w Katowicach. Współczesne Finanse 356: 157–69. [Google Scholar]

Figure 1.

The level of non-financial reporting depending on the size of the enterprise. * As the information for 2018–2020 is incomplete due to ongoing data collection and the Standards Report Registration process, the search on the report year filter is disabled for the years 2018 and 2019. This change was made to avoid any data or trend misinterpretations. 2018–2020 years—these reports were found using the other available filters, therefore, a total value is shown for this period. Source: owned elaboration based on (GRI n.d.) (24.11.20.).

Figure 1.

The level of non-financial reporting depending on the size of the enterprise. * As the information for 2018–2020 is incomplete due to ongoing data collection and the Standards Report Registration process, the search on the report year filter is disabled for the years 2018 and 2019. This change was made to avoid any data or trend misinterpretations. 2018–2020 years—these reports were found using the other available filters, therefore, a total value is shown for this period. Source: owned elaboration based on (GRI n.d.) (24.11.20.).

{kind=link}

Table 1.

Definitions of size of the entity.

| Enterprise Category | Headcount | Turnover | Balance Sheet Total |

|---|---|---|---|

| Organizations are classified as SMEs based on local regulations. In the absence of local regulations classification based on the EU definition for SMEs | |||

| SME | <250 | 50 million Euro or | 43 million Euro |

| For Large Enterprises and MNEs, GRI follows the EU definitions of size | |||

| Large | >250 | >50 million Euro or | >43 million Euro |

| MNE | >250 and multinational | >50 million Euro or | >43 million Euro |

Source: (GRI 2020).

Table 2.

International non-financial reporting standards.

| Name of the Standard/Issuing Institution | Reporting Area | Who Is It for? | Can It Be Implemented in the SME Sector? | |||

|---|---|---|---|---|---|---|

| Environmental Issues | Social and Employee Issues | Human Rights | Anti-Corruption | |||

| GRI Sustainability Reporting Guidelines (GRI Standards/GRI G4)—Global Reporting Initiative (GRI) | + | + | + | + | Business, government agencies, cities, social and educational organizations, regardless of size and industry. | Yes |

| Communication on Progress (COP)—UN Global Compact | + | + | + | + | The reporting system was created for the signatories of the 10 Principles of the Global Compact. They can be organizations employing at least 10 employees, representing various sectors of business, local government, and social organizations. | Yes, excluding micro-entities |

| International Integrated Reporting Framework—International Integrated Reporting Council (IIRC) | + | + | + | - | Enterprises | Yes |

| Guidance on Corporate Responsibility Indicators in Annual Reports UNCTAD—United Nations Conference on Trade and Development (UNCTAD) | - | + | - | + | Enterprises | Yes |

| KPIs for ESG European Federation of Financial Analysts Societies (EFFAS) and DVFA Society of Investment Professionals in Germany | + | + | + | + | The guidelines have been developed for all. | Recommended for companies listed on stock exchanges or issuing bonds. |

| Model Guidance on Reporting ESG Information to Investors Sustainable Stock Exchanges Initiative—the United Nations Sustainable Stock Exchanges (SSE) initiative | + | + | + | + | Stock exchanges around the world. | No |

| UN Guiding Principles Reporting Framework—Human Rights Reporting and Assurance Frameworks Initiative (RAFI) | + | + | + | + | Enterprises regardless of their size, location, sector and type of activity. | Yes |

| Principles for Responsible Investment (UN PRI)—United Nations (UN) | + | + | + | + | Institutional investors, signatories of the UN PRI initiative, which consists of 6 principles of responsible investment. | No |

| OECD Guidelines for Multinational Enterprises (OECD Guidelines for MNEs)—Organization for Economic Cooperation and Development, (OECD) | + | +. | + | + | Multinational enterprises, including companies or other entities established in several countries that enable them to coordinate their activities. | No |

| ISO 26000 Guidance on social responsibility—International Organization for Standardization (ISO) | + | + | + | + | Enterprises, non-profit organizations, administration, employers’ organizations, trade unions. Regardless of size or industry. | Yes |

Source: owned elaboration based on (PRI n.d.; UN Guiding Principles n.d.; SSE n.d.; EFFAS n.d.; UNCTAD n.d.; Integrated Reporting n.d.; UN Global Compact n.d.; GRI n.d.; PKN n.d.).

Table 3.

Development of non-financial reporting from 1999 to 2020.

| Report Year | All Reports | SME | MNE | Large | Percentage in All | ||

|---|---|---|---|---|---|---|---|

| SME | MNE | Large | |||||

| 1999–2003 | 542 | 19 | 145 | 378 | 3.51% | 26.75% | 69.74% |

| 2004 | 320 | 15 | 84 | 221 | 4.69% | 26.25% | 69.06% |

| 2005 | 446 | 30 | 104 | 312 | 6.73% | 23.32% | 69.96% |

| 2006 | 688 | 50 | 184 | 454 | 7.27% | 26.74% | 65.99% |

| 2007 | 1004 | 77 | 275 | 652 | 7.67% | 27.39% | 64.94% |

| 2008 | 1513 | 132 | 393 | 988 | 8.72% | 25.97% | 65.30% |

| 2009 | 1998 | 203 | 499 | 1296 | 10.16% | 24.97% | 64.86% |

| 2010 | 2650 | 275 | 643 | 1732 | 10.38% | 24.26% | 65.36% |

| 2011 | 3960 | 425 | 1012 | 2523 | 10.73% | 25.56% | 63.71% |

| 2012 | 4708 | 521 | 1251 | 2936 | 11.07% | 26.57% | 62.36% |

| 2013 | 5326 | 588 | 1435 | 3303 | 11.04% | 26.94% | 62.02% |

| 2014 | 5965 | 660 | 1654 | 3651 | 11.06% | 27.73% | 61.21% |

| 2015 | 6458 | 718 | 1888 | 3852 | 11.12% | 29.24% | 59.65% |

| 2016 | 7117 | 745 | 1986 | 4386 | 10.47% | 27.91% | 61.63% |

| 2017 | 7330 | 833 | 2031 | 4466 | 11.36% | 27.71% | 60.93% |

| Average 2018–2020 * | 4573 | 792 | 1188 | 2592 | 17.33% | 25.99% | 56.69% |

| ∑ 2018–2020 * | 13,719 | 2377 | 3565 | 7777 | 17.33% | 25.99% | 56.69% |

| ∑ 1999–2020 | 63,744 | 7668 | 17,149 | 38,927 | 12.03% | 26.90% | 61.07% |

* As the information for 2018–2020 is incomplete due to ongoing data collection and the Standards Report Registration process, the search on the report year filter is disabled for the years 2018 and 2019. This change was made to avoid any data or trend misinterpretations. 2018–2020 years—these reports were found using the other available filters, therefore, a total value is shown for this period. Source: owned elaboration based on (GRI n.d.) (24.11.20.).

Table 4.

Reporting in small and medium-sized enterprises using GRI 1999–2020 (in percentage).

| Report Year | SME Reports | GRI–G1 | GRI–G2 | GRI–G3 | Non GRI | GRI–G3.1 | GRI–G4 | GRI Standards | Citing–GRI |

|---|---|---|---|---|---|---|---|---|---|

| 1999–2003 | 19 | 9 (47.37%) | 6 (31.58%) | 4 (21.05%) | |||||

| 2004 | 15 | 11 (73.33%) | 3 (20%) | 1 (6.67%) | |||||

| 2005 | 30 | 28 (93.33%) | 2 (6.67%) | ||||||

| 2006 | 50 | 37 (74%) | 9 (18%) | 3 (6%) | 1 (2%) | ||||

| 2007 | 77 | 8 (10.39%) | 62 (80.52%) | 6 (7.79) | 1 (1.3%) | ||||

| 2008 | 132 | 1 (0.76%) | 118 (89.39%) | 9 (6.82%) | 4 (3.03%) | ||||

| 2009 | 203 | 183 (90.15%) | 14 (6.9%) | 6 (2.96%) | |||||

| 2010 | 275 | 242 (88%) | 25 (9.09%) | 8 (2.91%) | |||||

| 2011 | 425 | 172 (40.47%) | 98 (23.06%) | 31 (7.29%) | 24 (5.65%) | ||||

| 2012 | 521 | 200 (28.06%) | 143 (27.45%) | 139 (26.68%) | 38 (7.29%) | ||||

| 2013 | 588 | 165 (38.39%) | 190 (32.31%) | 172 (29.25%) | 13 (2.21%) | 48 (8.16%) | |||

| 2014 | 660 | 97 (14.07%) | 228 (34.55%) | 126 (19.09%) | 145 (21.97%) | 64 (9.7%) | |||

| 2015 | 718 | 38 (5.29%) | 246 (34.26%) | 65 (9.05%) | 296 (41.23%) | 73 (10.17%) | |||

| 2016 | 745 | 327 (43.89%) | 336 (45.1%) | 3 (0.4%) | 79 (10.6%) | ||||

| 2017 | 833 | 455 (54.62%) | 259 (31.09%) | 49 (5.88%) | 70 (8.4%) | ||||

| 1999–2017 | 5291 | 9 (0.17%) | 91 (1.72%) | 1386 (26.2%) | 1753 (33.13%) | 533 (10.07%) | 1049 (19.83%) | 52 (0.98%) | 418 (7.9%) |

| 2018–2020 * | 2377 | 844 (35.51%) | 110 (4.63%) | 1253 (52.71%) | 170 (7.15%) | ||||

| 1999–2020 | 7668 | 9 (0.12%) | 91 (1.19%) | 1386 (18.08%) | 2597 (33.87%) | 533 (6.95%) | 1159 (15.11%) | 1305 (17.02%) | 588 (7.67%) |

* As the information for 2018–2020 is incomplete due to ongoing data collection and the Standards Report Registration process, the search on the report year filter is disabled for the years 2018 and 2019. This change was made to avoid any data or trend misinterpretations. 2018–2020 years—these reports were found using the other available filters therefore, a total value is shown for this period. Source: owned elaboration based on (GRI n.d.) (24.11.20.).

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Krawczyk, P. Non-Financial Reporting—Standardization Options for SME Sector. J. Risk Financial Manag. 2021, 14, 417. https://doi.org/10.3390/jrfm14090417

AMA Style

Krawczyk P. Non-Financial Reporting—Standardization Options for SME Sector. Journal of Risk and Financial Management. 2021; 14(9):417. https://doi.org/10.3390/jrfm14090417

Chicago/Turabian StyleKrawczyk, Patrycja. 2021. "Non-Financial Reporting—Standardization Options for SME Sector" Journal of Risk and Financial Management 14, no. 9: 417. https://doi.org/10.3390/jrfm14090417