The corporate financial soundness can be analyzed using financial ratios, in a rather similar way than a person’s health using a blood analysis. Financial ratios are proportions of relative magnitudes that use two or more figures taken from financial statements. When compared to a given standard, the observer can tell whether the company is more likely to experience some event (provided everything remains constant). A good set of ratios, carefully chosen and properly analyzed, can even give an expert an accurate idea of how much time could the firm live before entering a financial distress period and, eventually, go bankrupt. The interest from both industry and scholars on this topic gained intensity after several rather expensive corporate failures from 2000 onward.

This topic has been largely addressed by the scholar community, addressing it using different models and techniques, from traditional techniques, such as discriminant or logit analysis, to modern deep-learning schemes. The debate has substantially been focused on the following three questions: (1) what is the optimal ratio set for a given industry? (2) for how long can a given model be considered accurate and reliable prior to a bankruptcy event? and (3) how can the problems associated with unbalanced datasets, lack of variates’ normality, or large amounts of financial data disconnected from their—perhaps relevant—market information? The models proposed so far featured quite different approaches, trying to address some of the constraints detected prior to each one in this field. Thus, since the first logit or regressive models were presented, more techniques that are progressively more powerful have been incorporated, such as neural networks or business intelligence algorithms. However, parametric multivariate approaches have repeatedly faced two problems—first, the fact that a given set of financial information accomplishes the normality condition and, second, the datasets are often plenty of information about alive firms but lack the essential data about enterprises who yet expired. This problem is even more critical when the information is taken in a relative timeline, totally disconnected from the events that possibly affected the historical records for any firm in the dataset. As a result, the models yet known are good classifying firms that most likely will go bankrupt in the medium term, a maximum of four years.

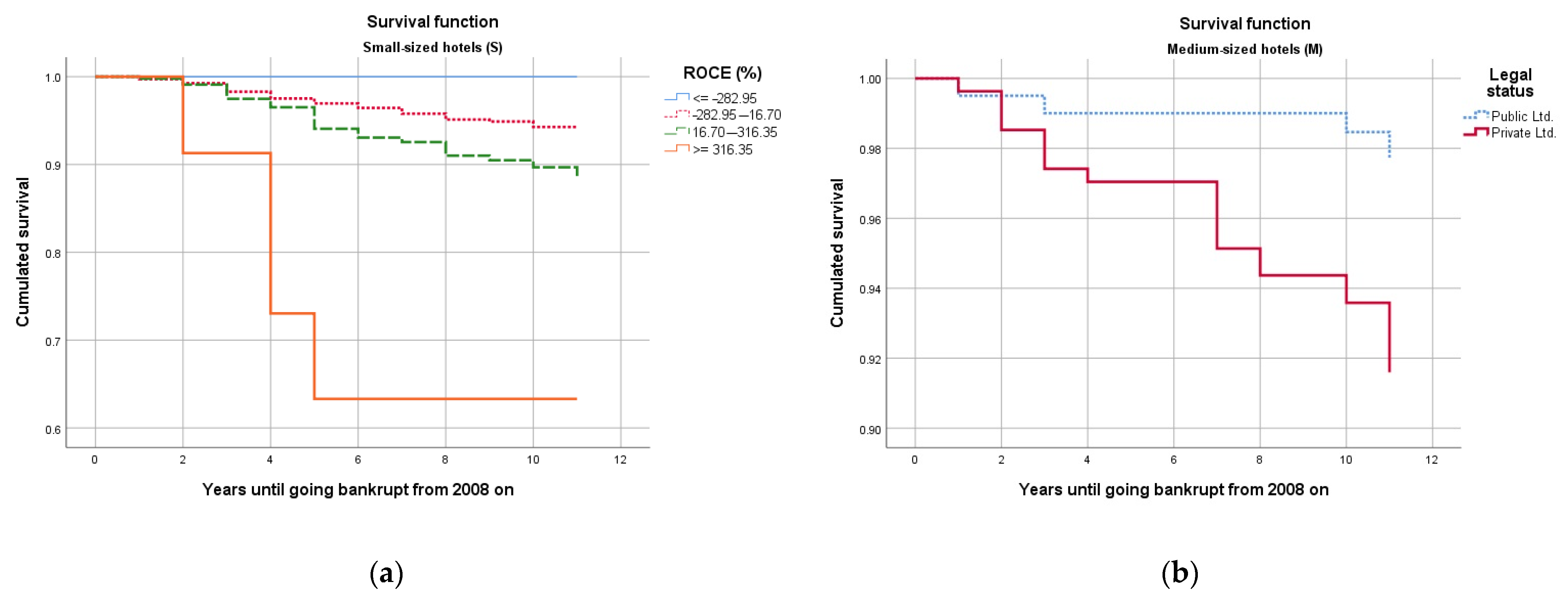

Furthermore, because 2008 was the year when an unprecedented economic stagnation began for the whole tourism industry in Spain, we considered it a relevant starting point to go forward in time, analyzing the ratios of the companies at that point in 2008 and stating if it had a significant influence on whether the hotel had survived the crisis.

Consequently, as we were speculating with the theory of a long-term effect of any of the ratios in the survival function of the firms when a crisis arises, we stipulated our hypotheses in the following way:

1.1. Models and Techniques Used in Corporate Failure Prediction

Analyzing the financial distress of companies has been a challenge widely tackled by scientists, due to its importance when it comes to evaluating loans, insurances, and any sort of operation subject to the fact that the enterprise is still open for business in the stipulated time. The modern approaches early in de seventies pointed out very soon the usefulness of the ratios as predictors of the companies’ financial distress. Historically, the first attempts to provide scientific insights over bankruptcies and their prediction focused on different ratio sets, often too diffuse and too dependent on large datasets. In particular, the outstanding work created by Altman [

3] in 1968 was widely applied in many sectors, whereas it was designed for manufacturing corporations through a Z-score evaluation concerning a set of ratios. Dividing that score into three areas, namely a distress zone, a grey zone, and a safe zone, the model became very popular among practitioners and scholars for decades. Moreover, Johnson [

4] summarized and proposed an interesting set of relevant ratios in 1979, again based on manufacturing and retailers’ data. After screening 61 financial ratios, Johnson found that a factor analysis grouped them up into eight categories, highlighting the fact that there are ratios that belong to a similar group, yet empirically determined.

These preliminary approaches were completed very soon using other models and statistics, and comparing them to each other in pursuit of the optimal way of evaluating different ratio sets. Several important advances in this side were produced in the 1990s when multinomial logit methods [

5] or neural networks [

5,

6] seemed pretty promising. Actually, Johnsen and Melicher [

5] pointed out that it is better to understand the classification using the distress zone as a continuum, rather than only looking for a two-class classifier (i.e., bankrupt versus non-bankrupt). In the same vein, Atiya [

6] proposed using neural networks as a way to better analyze the ratio sets and include novel indicators that increased the accuracy of the forecasts up to three years in advance.

Later on, new comparisons were then performed in the search for an optimal model, but ultimately, there seemed to be no single specific standard to compare, so the issue generated several ways for comparing different options for bankruptcy prediction. An example of this can be found in the case of using linear discriminant analysis by Altman himself and Varetto [

7]. On the opposite side, from the ratio-approach academicians, Mossman et al. [

8] suggested in 1998 that although ratios are a good predictor for the very short term, none of the models proposed so far were accurate enough beyond a two-year horizon. Despite this fact, in 2007, Sun [

9] proposed including non-traditional variables (e.g., abnormal stock returns) and using a hazard model that outperformed the reference classification model. In 2008, Agarwal and Taffler compared two approaches—the Z-score model against market-based models—and concluded that every approach captures different information about corporate failure, but “neither method subsumes the other” [

10].

It can be noted that the first comprehensive studies had the merit of establishing the basics for the forthcoming approaches, given the technology and techniques of the times. The main goal was then getting the best classification model for telling whether a given company could go bankrupt with anticipation enough to avoid it or, at least, to issue a warning to lenders, customers, employees, or shareholders. On a slightly different approach, this work evaluates the relative importance of several of the traditional ratios and seeks how related they are, in the long term, with bankruptcies already known.

In the last two decades, other models emerged, proposing binary classification [

11], Malahanobis distance [

12], or multiperiod prediction [

13] as more fit techniques for predicting corporate failure. These methods were proposed along with the evolution of neural networks in the shape of fuzzy logic, also at the same time of quite interesting works comparing those models. It is remarkable how outperformed a radial basis function network compared to other classification systems [

14], which is consistent with Kim’s findings. He suggested using artificial neural networks as the most accurate classifier compared to logistic or discriminant multivariate approaches, or event to support vector machine [

15], which solves the classification problem using hyperplanes. In recent years, the proposed models have been using genetic algorithms [

16] or deep learning techniques [

17], mainly black-box approaches to achieve the objective of optimal classifications and, eventually, forecasts. Chou et al. [

16] divided their 600-company dataset into three groups, according to their respective industries, the selected year, and the company capital. Adapting their assumption to our case, we have also split the sample into three groups. Moreover, Mai et al. [

17] introduce a relevant concept for our purposes, the fact that economic crises are relevant for bankruptcy prediction. They actually point out 2008 as “the Great Recession,” which is in line with our work assumptions.

However, in spite of the large effort of research put into this topic, it is remarkable how few papers have addressed two relevant topics still under debate—(1) the unbalanced datasets commonly used in the research so far and (2) the valid anticipation for prediction. In the first issue, it is important to bring forward the works of Le et al. [

18,

19], who proposed compensating the unbalanced datasheets when using complex algorithms, due to the fact that there were always many more non-bankrupt companies in the datasets than firms that had gone bankrupt. This concern has also been addressed by Zoričák et al., who used three algorithms in turn [

20]. This paper approaches the issue in a different way, addressing it either in the technique or the method, by combining the relatively new survival analysis with a time-fixed data scheme.

On the other hand, the classification methods—regardless of the technique—do not seem to be able of improving the time period within the forecast is valid and reliable. Yet, in 1998, Mossman et al. pointed out that the models can predict bankruptcy only two years in advance [

8], which only improved up to three years when using multiperiod prediction [

13], but still certainly short; sadly, it is interesting to remark at this point how the most recent literature underlines logistic regressions or neural network as superior methods compared to other models [

21]. This work does not provide a comprehensive classification model; however, it can help improving part of the systems already provided, underlining the relative importance of several ratios when trying to build a long-term classification model, accurate for five or more years, as illustrated by Altman et al. [

21].

Irrespective of the scholarly trend into which any study falls (i.e., finding the failure and its symptoms versus comparing the classification systems accuracy [

14]), the ultimate resource to be taken into consideration is the ratio dataset. Despite the fact that other mixed approaches have been proposed, the specific financial ratio analysis is still a very challenging and active topic for there are continuous outcomes concerning the relationship with the financial health of a given company. In addition, there is evidence of a strong relationship between several ratios and corporate failure. There are a number of ratios mentioned in the literature that could play a different role in this process, and they are specially surveyed by those who, in one way or another, need to foreknow the expected life of any company, such as lenders, insurance companies or public institutions. However, the model used often changes depending on the country [

22] or could be influenced by the nature of the activity of the enterprise [

23]. Those aspects have been seldom approached by academicians or practitioners, and it is worthwhile bringing forward those who underpinned this issue. On one side, Kliestik et al. presented a quite original way of grouping up ratios, using cluster analysis rather than like Johnson’s [

4] factor analysis. Moreover, they crossed the ratios and the countries where they are commonly used for calculating financial distress, and it turned out that depending on the country (or political background), the ratios used are different. On a different topic, Pech et al. [

23] used a well-balanced 60-enterprise sample for analyzing the bankruptcies in the same period of the present study. One of their outcomes was that there were weaker classification systems when the dataset mixes companies from different industries. That is the reason for this study to focus on a single homogenous service (lodging).

Using financial ratios for getting diagnostics about financial distress or the likelihood of a corporate failure has been a boosting topic in the last two decades, associated with new algorithms and techniques, not to mention the improved capabilities of the technology for managing large datasets and perform complex calculations. Many of the analyses use a single sound technique for improving the accuracy of the models proposed or rather propose new models. In 2000, Laitinen and Laitinen [

24] proposed a solution for the issue about the normality of the variables involved in many of those analyses, using Taylor’s series expansion instead of a logistic or exponent function. At this point, it is remarkable that the model proposed in this research overcomes the problem of data normality, due to the fact that the survival analysis is not a parametrical test and, consequently, does not assume a specific distribution of the data.

The logit model used so far also was improved in 2010 by Li and Liu [

25], who proposed to use dynamic loadings instead of constant. Bahiraie et al. [

26] proposed another approach in 2011, the dynamic geometry approach, which is really promising, but it seems to have no further improvements on that side so far. De Andrés et al. [

27] approached the topic in a different way and suggested that it is not the ratio, but its deviation from an industry standard, which really matters for classifiers, suggesting several interesting ideas to the scholarly debate. In 2017 Tian and Yu [

28] suggested a different set of ratios for Japan and several European countries, providing a quite interesting insight into how different predictors could be depending on the country where the firm is located. This seems to be confirmed by the work performed by Kliestik et al. [

22], which suggests different preferences depending on the country when it comes to evaluate firms and predict their bankruptcy. The latest improvements addressing issues in this matter came from Balina and Idasz-Balina [

29], who proposed to take into consideration two so-called stimulants—current assets to total assets ratio and quick liquidity ratio.

{kind=link}

{kind=link}