Abstract

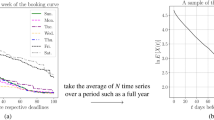

The price reaction to a single transaction depends on transaction volume, the identity of the stock, and possibly many other factors. Here we show that, by taking into account the differences in liquidity for stocks of different size classes of market capitalization, we can rescale both the average price shift and the transaction volume to obtain a uniform price-impact curve for all size classes of firm for four different years (1995–98). This single-curve collapse of the price-impact function suggests that fluctuations from the supply-and-demand equilibrium for many financial assets, differing in economic sectors of activity and market capitalization, are governed by the same statistical rule.

This is a preview of subscription content, access via your institution

Access options

Subscribe to this journal

Receive 51 print issues and online access

$199.00 per year

only $3.90 per issue

Buy this article

- Purchase on Springer Link

- Instant access to full article PDF

Prices may be subject to local taxes which are calculated during checkout

Similar content being viewed by others

References

Hasbrouck, J. Handbook Stat. 14, 647–692 (1996).

Hausman, J. A. & Lo, A. W. J. Finan. Econ. 31, 319–379 (1992).

Chan, L. K. C. & Lakonishok, J. J. Finance 50, 1147–1174 (1995).

Dufour, A. & Engle, R. F. J. Finance 55, 2467–2498 (2000).

Farmer, J. D. Slippage 1996 (Predictions Co. Tech. Rep., Santa Fe, New Mexico, 1996); http://www.predict.com/jdf/slippage.pdf

Torre, N. BARRA Market Impact Model Handbook (BARRA, Berkeley, California, 1997).

Kempf, A. & Korn, O. J. Finan. Mark. 2, 29–48 (1999).

Chordia, T., Roll, R. & Subrahmanyam, A. J. Finan. Econ. 65, 111–130 (2002).

Plerou, V., Gopikrishnan, P., Gabaix, X. & Stanley, H. E. Phys. Rev. E 66, 027104 (2002).

Lee, C. M. C. & Ready, M. J. J. Finance 46, 733–746 (1991).

Daniels, M., Farmer, J. D., Iori, G. & Smith, D. E. Preprint http://xxx.lanl.gov/cond-mat/0112422 (2001).

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing financial interests.

Rights and permissions

About this article

Cite this article

Lillo, F., Farmer, J. & Mantegna, R. Master curve for price-impact function. Nature 421, 129–130 (2003). https://doi.org/10.1038/421129a

Issue Date:

DOI: https://doi.org/10.1038/421129a

This article is cited by

-

Deep learning algorithms for hedging with frictions

Digital Finance (2023)

-

A Finite Difference Scheme for Pairs Trading with Transaction Costs

Computational Economics (2022)

-

Negative selection—a new performance measure for automated order execution

Journal of Mathematics in Industry (2021)

-

An empirical behavioral order-driven model with price limit rules

Financial Innovation (2021)

-

Regularized stochastic dual dynamic programming for convex nonlinear optimization problems

Optimization and Engineering (2020)

Comments

By submitting a comment you agree to abide by our Terms and Community Guidelines. If you find something abusive or that does not comply with our terms or guidelines please flag it as inappropriate.